DC Discusses: Hooking onto commercial success - the sensation of global seafood

Date

January 28, 2020 • 7 min read

Despite geopolitical uncertainty the global food sector experienced an increase in investment activity over the last 12 months (a trend which is expected to continue) and during this period, one of the more interesting sub-sectors has been seafood.

Buyers and sellers across international markets are benefitting from an increasing consumer appetite which is driving profit growth for key players and spurring interest in M&A activity.

The broader seafood landscape is now being significantly impacted by the sustainable and ethical behaviours of consumers and a rise in disposable incomes in developed markets. Growth in profitability has, in turn, meant that larger sector operators continue to seek opportunities to unlock different parts of the supply chain – often via M&A – to harness competitive advantage.

The below graph illustrates the strong levels of activity across the sector since 2013, with a significant focus on European assets which are increasingly attracting both trade and PE buyers.

![]()

The production growth of fish alone is expected to increase by 10% globally between 2018 to 2027 – clearly outpacing global population growth and posing a significant opportunity for investors. In 2018, fish consumption only accounted for 5% of global protein consumption, however, it’s estimated that this will increase by 3% in the period 2018 to 2027 [1]. As the consumption of fish and seafood steadily increases, we expect this sector as a broader protein category to continue gaining positive traction with consumers and investors alike.

So how can investors capitalise on the opportunities in the seafood market? DC Advisory’s Global Consumer, Leisure & Retail team explores >

In the era of the environmentally and health-conscious consumer, the global food market has seen consumers transform their palate from traditional proteins such as red meat or poultry, to pescatarian or plant-based choices. Aquaculture or aquafarming has played a material role in meeting this demand which has been supported by improved farming practices and better quality products. The increased penetration of Asian, more seafood-based cuisine, in Western Europe and North America has led to a wider knowledge of fish and seafood dishes.

Millennials are driving this trend across numerous markets; animal welfare issues, environmental impacts and food sourcing are at the forefront of their decision-making process [2] – which has meant that the sustainability debate continues to unfold in households, offices and parliaments worldwide.

Many argue that the environmental impact imposed by the meat industry far outweighs that of the seafood market, which claims to produce a smaller carbon footprint compared to other animal proteins – hence the debate.

As consumers are increasingly influenced by sustainability objectives, stakeholders across the global seafood market – such as retailers, governments and consumers – are now demanding that significantly higher certification standards are met, resulting in more and more producers adhering to traceability procedures and fishery compliance standards. With this trend, operators and consumers alike, now more than ever, are playing a pivotal role in securing the future of seafood and oceanic health.

The emphasis on shifting legal frameworks and enforcing new stricter standards may result in further market consolidation as smaller players are forced to become more compliant – this may cause a knock-on effect due to cost implications, thus allowing bigger players to takeover less well-invested and capitalised assets.

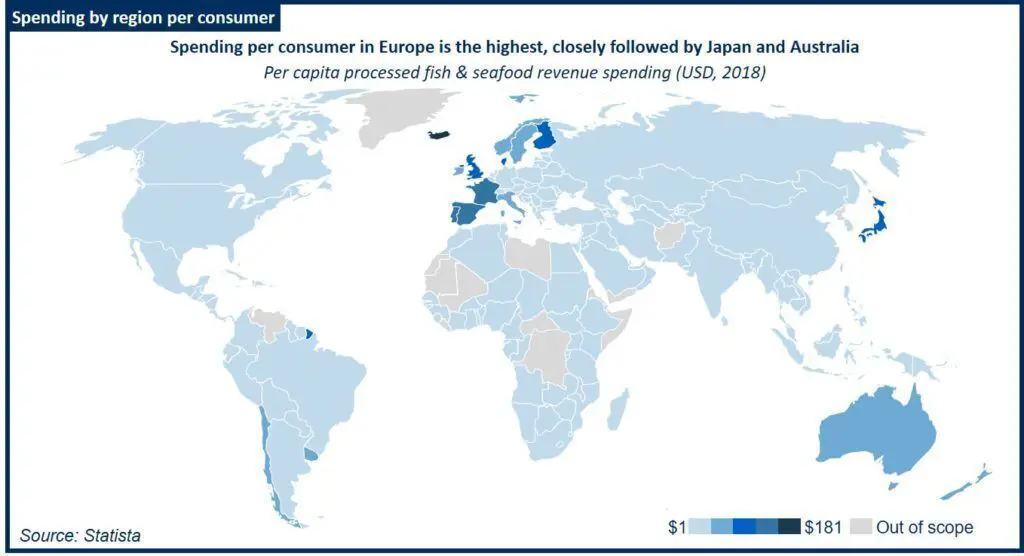

In addition to the rising transition towards healthier diets, increasing disposable incomes in a higher proportion of countries continues to influence seafood consumption. Not only do consumers have more choice and access to seafood products, seafood producers have responded to this demand and are increasingly equipped to export stock around the world.

In short, spending per capita on seafood directly correlates with the prosperity of the consumers (see below).

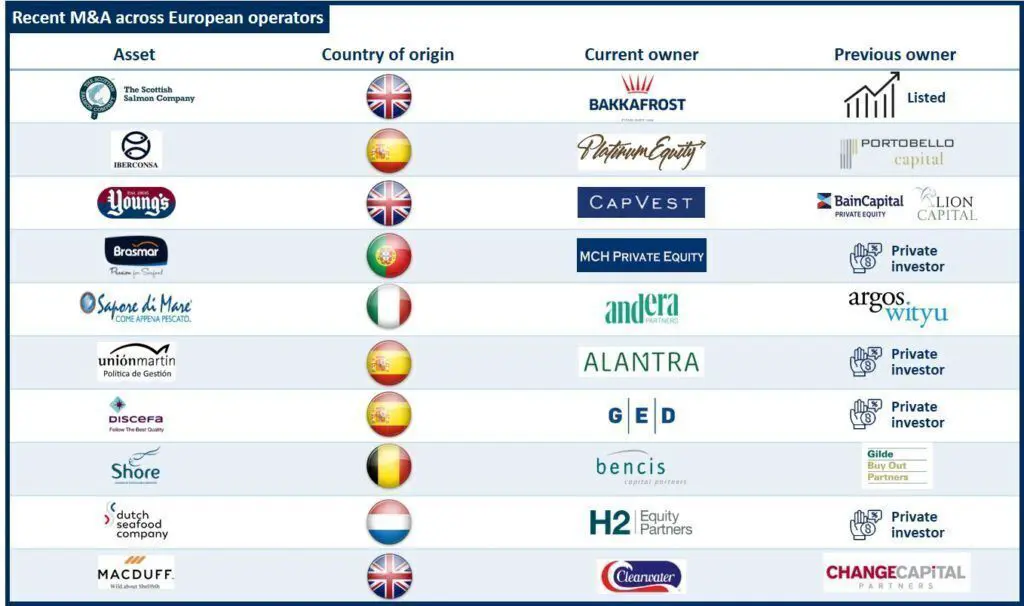

Due to these positive macro and industry dynamics, private equity investors are increasingly attracted to the seafood sector. This is particularly evident across Europe, with portfolio managers either purchasing new assets from previous private equity owners, or buying out assets directly from operating shareholders. Recent M&A activity across Europe includes:

Asia, on the other hand, has experienced different trends. Increasing consumer appetite provide significant opportunities to operators with established industry relationships and exporting channels.

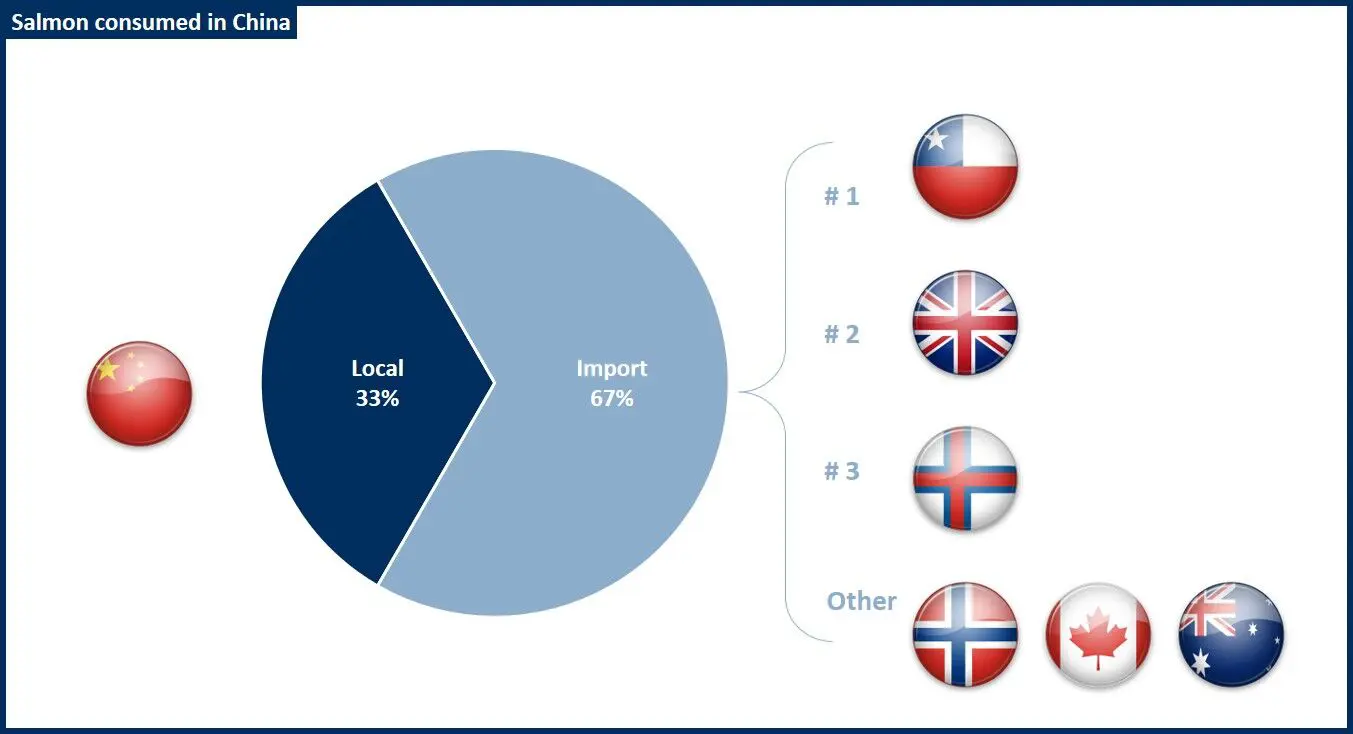

Despite China’s consumption of domestically-produced seafood declining during the last 12 months, European and US-based producers have gained greater access to the market to satisfy domestic demand, providing higher quality products at a premium price. China’s demand for seafood, in particular salmon, continues to grow and is projected to increase by 25% per annum.

The below chart illustrates China’s salmon consumption rates and the proportion of imported and locally sourced produce.

Similarly, the emergence of a middle class with rising purchase power is increasingly evident across the BRIC economies. As we continue to see growth in global consumption of more premium seafood, we can expect to see solid revenue growth and profitability within the seafood sector for the foreseeable future.

Japanese and other Asian seafood leaders, however, are not only focusing their expansion efforts on China and developing countries, but have been also looking closely for opportunities in the Americas and Europe to complement their offering, gain access to new markets and/or increase their production or processing volume. The US players on the other hand, have remained much more concentrated on their domestic market driven by differing regulations and varied consumer tastes – a trend we expect to continue.

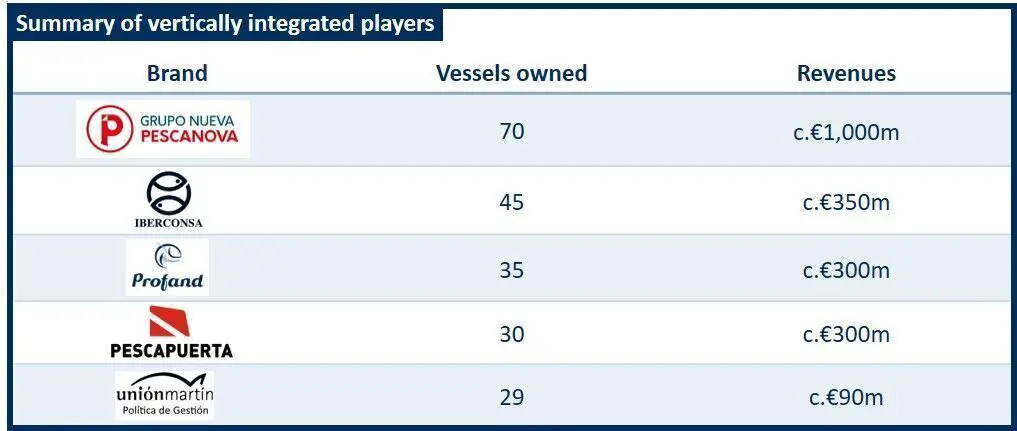

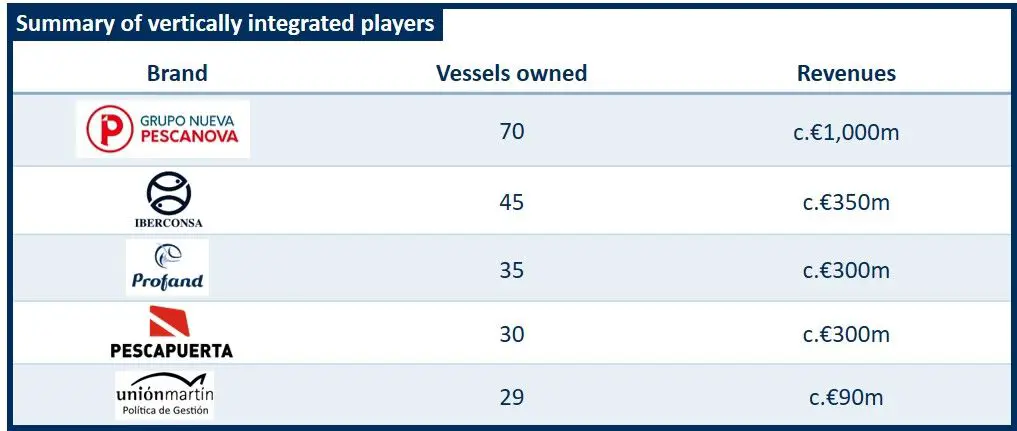

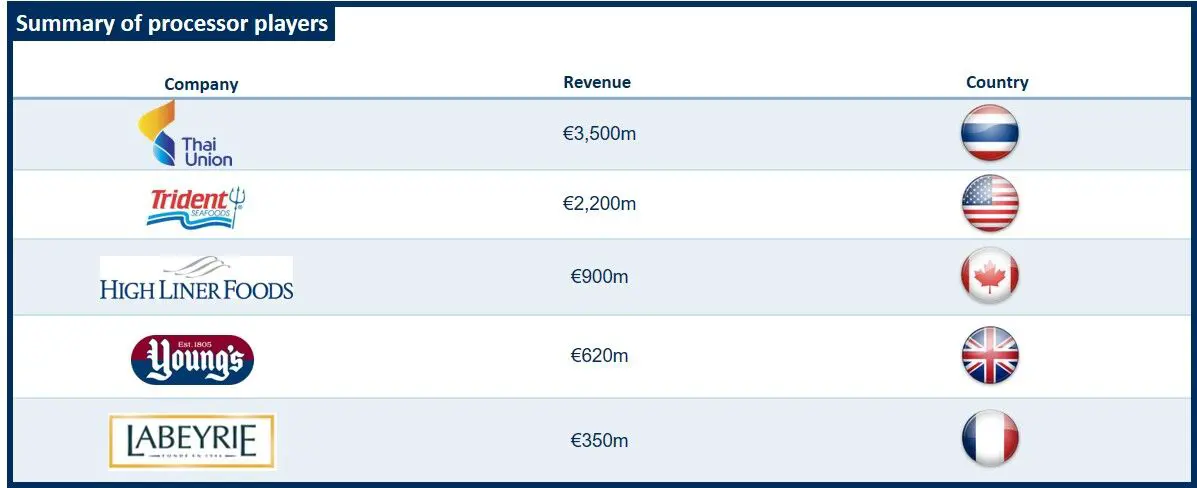

The global seafood industry is divided into vertically integrated operators that own and control all functions along the value chain and processing specialists that focus on providing the best products swiftly to their customers. Vertically integrated players manage elements such as producing fish feed, farming, processing, production and supply to:

Below are examples of seafood players who have done just this – owning vessel fleets for fishing and processing plants, with some now focusing on trading and other components within the supply chain. Also below is an overview of the seafood M&A transactions completed during 2019, demonstrating the trends towards vertical integration, in addition to a summary of the key processors who are gaining traction across the market.

![]()

Asia, on the other hand, has experienced different trends. Increasing consumer appetite provide significant opportunities to operators with established industry relationships and exporting channels.

Despite China’s consumption of domestically-produced seafood declining during the last 12 months, European and US-based producers have gained greater access to the market to satisfy domestic demand, providing higher quality products at a premium price. China’s demand for seafood, in particular salmon, continues to grow and is projected to increase by 25% per annum.

The below chart illustrates China’s salmon consumption rates and the proportion of imported and locally sourced produce.

Similarly, the emergence of a middle class with rising purchase power is increasingly evident across the BRIC economies. As we continue to see growth in global consumption of more premium seafood, we can expect to see solid revenue growth and profitability within the seafood sector for the foreseeable future.

Japanese and other Asian seafood leaders, however, are not only focusing their expansion efforts on China and developing countries, but have been also looking closely for opportunities in the Americas and Europe to complement their offering, gain access to new markets and/or increase their production or processing volume. The US players on the other hand, have remained much more concentrated on their domestic market driven by differing regulations and varied consumer tastes – a trend we expect to continue.

The global seafood industry is divided into vertically integrated operators that own and control all functions along the value chain and processing specialists that focus on providing the best products swiftly to their customers. Vertically integrated players manage elements such as producing fish feed, farming, processing, production and supply to:

Below are examples of seafood players who have done just this – owning vessel fleets for fishing and processing plants, with some now focusing on trading and other components within the supply chain. Also below is an overview of the seafood M&A transactions completed during 2019, demonstrating the trends towards vertical integration, in addition to a summary of the key processors who are gaining traction across the market.

![]()

Vertically integrating helps to capitalise on notable sector trends and provides the opportunity for seafood producers to pitch their product at the cost that is the most attractive to consumers. This enables the business to remain resilient in less prosperous times, and can help to maximise long-term profitability and competitive advantage.

Additionally, vertical integration can be critical to control the product quality and to ensure costs are effectively maintained. Conversely, other market participants argue that specialising in processing is more important, particularly when this has been at the core of operations – this approach enables the business to best service its retail and food service customers and is able to make swift adjustments based on changing consumer behaviours and demand. An additional argument for the non-integrated commercial approach is that the supply chain is typically very flexible – enabling processing specialists to shift from another supplier in the instance of quality problems.

The trends highlighted above will continue to impact the attractiveness of the global seafood sector. To capitalise on this growth, investors and operators are urged to remain up to date with market activity and to understand how consumer behaviours, commercial strategies and sustainability continues to transform the landscape.

We expect continued M&A activity not only in Europe but also in Asia, LATAM and the US as private equity owned assets reach the end of the investment cycle, and privately owned businesses attract interest from global leaders from across the sector.

Should you have any questions regarding these trends, DC Advisory’s Global Consumer, Leisure & Retail team would be delighted to discuss these with you in more detail.

THIS PUBLICATION IS NOT A RESEARCH REPORT, SHOULD NOT BE CONSTRUED AS ONE AND HAS NOT BEEN PRODUCED BY A RESEARCH ANALYST. ADDITIONALLY, THIS PUBLICATION DOES NOT CONSTITUTE OR FORM PART OF, AND SHOULD NOT BE CONSTRUED AS, AN OFFER TO SELL OR ISSUE, A SOLICITATION OF ANY OFFER TO BUY, OR A RECOMMENDATION WITH RESPECT TO, ANY SECURITIES. ACCORDINGLY, YOU SHOULD NOT BASE ANY INVESTMENT DECISION ON THIS PUBLICATION, AND SHOULD OBTAIN INDEPENDENT FINANCIAL, LEGAL, AND TAX ADVICE WITH RESPECT TO ANY SUCH INVESTMENT DECISION.

DC ADVISORY DOES NOT MAKE ANY EXPRESS OR IMPLIED REPRESENTATION OR WARRANTY AS TO THE ACCURACY OR COMPLETENESS OF THE INFORMATION CONTAINED HEREIN AND SHALL HAVE NO LIABILITY TO THE RECIPIENT OR ITS REPRESENTATIVES RELATING TO OR ARISING FROM THE USE OF THE INFORMATION CONTAINED HEREIN OR ANY OMISSIONS THEREFROM.

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.