DC Discusses: Medtech ‘new normal’ brings new opportunities in 2023

Date

3 min read

On 7-9 Feb 2023, DC Advisory’s global Healthcare team attended MD&M West - one of the largest medical device conferences in North America. The conference hosted 46,000 attendees[1], including medtech professionals, medical OEM suppliers and private equity sponsors for a three-day forum, providing key insights and the latest advancements in the sector.

At the event, much was discussed around the performance of the medtech / medtech CDMO sector’s performance over the past two years, and how this has impacted M&A activity, investment appetite and valuation trends. DC Advisory US’ medtech expert, Managing Director Manish Gupta, reflects on discussions at the event, and shares key trends and insights to note for 2023 >

The medtech ‘new normal’

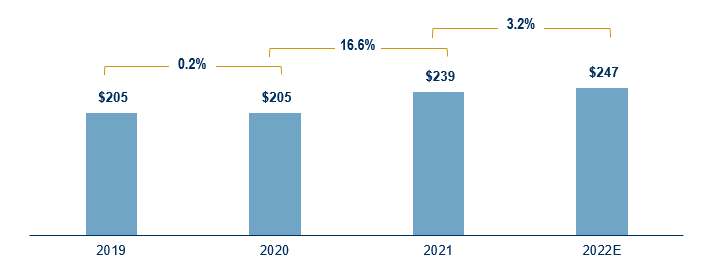

Our conversations with a number of operating companies and private equity groups suggested that medtech businesses seem to have overcome Covid-19 related disruptions, both on the demand and cost sides of P&L. Overall, medtech has successfully adapted to a ‘new normal’ operating environment, which, combined with impressive revenue growth (see Fig 1 below), has reinforced investment interest and robust valuations.

Fig. 1: Medtech revenue growth ($1B)

Company Filings; With respect to 2022 Revenue Growth Estimates: Copyright © 2023, S&P Global Market Intelligence (and its affiliates, as applicable)

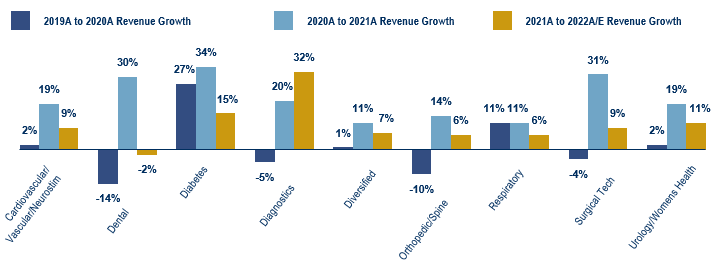

Interestingly, while 2022 growth rates came down from 2021 levels, virtually every major sector within medtech posted above-average growth rates (see Fig 2 below), pointing to continued post-Covid 19 recovery. Specifically:

Fig.2: Medtech performance by therapeutic area

Company Filings; With respect to 2022 Revenue Growth Estimates: Copyright © 2023, S&P Global Market Intelligence (and its affiliates, as applicable)

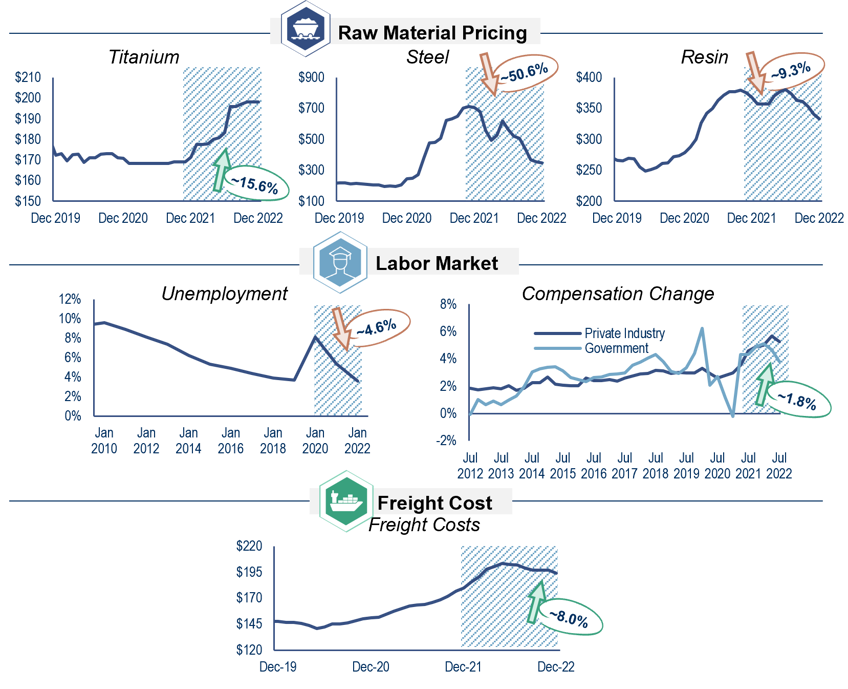

On the cost side, supply chain issues that businesses experienced during 2020 through to 2021 appear to be resolving. In addition, raw material pricing has come down from the pandemic induced highs (see Fig 3). However, labor shortages still pose challenges as unemployment remains historically low compared to previous years, putting pressure on profitability and consequently valuation.

Fig. 3: Sector cost drivers

Source: BLS.gov and FRED Economic Data as of January 19, 2023

We do want to raise a red flag around progressively increasing inventory with medical device companies as shown in Fig 4 below. While the pandemic required OEMs to build up inventory to mitigate any supplier related disruption, we anticipate that over time the OEMs will revert to longer-term historical averages and it may have a bearing on near-to-medium term product demand from suppliers putting pressure on top line growth for suppliers, which may in turn impact valuation.

Fig. 4: Inventory change for medtech OEMs

Source: Company Filings

Key M&A / investment trends to note:

Medtech CDMOs should remain at the top of mind for private equity and strategic acquirors as these companies have highly attractive organic growth and margin profile, very sticky customer base and limited-to-no clinical and regulatory risk.

To discuss the outputs in more detail, or for more information on medical device contract manufacturing and development landscape, please contact Manish Gupta >

[1] MDDI, an industry organization, the event had record attendance this year with over 16,000 attendees from medical device sector and non-medical attendees at over 30,000.

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.