DC Discusses: The real estate and healthcare real assets lending market – is debt the new equity?

Date

4 min read

Higher interest rates, upcoming credit maturities and a constellation of new debt funds have forged a new reality for the real estate and healthcare real assets lending market – one where debt is reaching pre-COVID-19 equity return levels. As sponsors look to manage covenants with value erosion concerns, is debt the new equity?

This new reality comprises several factors:

DC Advisory’s UK Real Estate and Healthcare team explores this new lending environment >

Volatility triggers change in valuation trends…

One can make the case that pre-COVID-19 was the peak of the real estate and healthcare real assets debt, where financing was still cheap, valuations were at an all-time high, and debt returns were low.[i]

Fast forward to 2023, interest rates have increased in the pandemic aftermath. We believe equity valuations remain uncertain and have not yet adjusted to the new environment, creating a window of opportunity for direct lenders[ii]. As a result, investing in equity generally carries a higher risk, while debt may provide up to double digit[iii] returns with lower risk.

On a risk-adjusted basis, sponsors consider debt returns more attractive than equity returns, explaining the leap of faith that traditional equity players are taking into credit strategies.[iv]

Shift in investor appetite…[v]

Post-COVID-19, high-street banks have shown a strong and consistent interest in real estate and healthcare real assets debt lending. Traditional debt and private equity funds have also been ramping up their debt strategies.

However, the level of appetite for real estate and healthcare real assets debt lending varies depending on the type of company and asset involved.

Overall, the real estate and healthcare real assets debt market remains dynamic and subject to shifting investor preferences. We explore the new lending environment below.

A new lending environment…

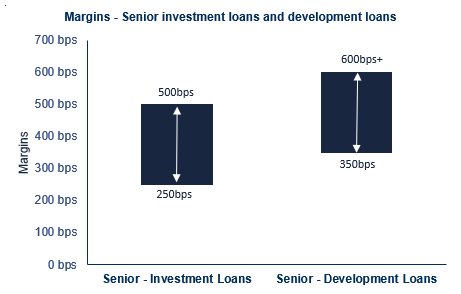

Whilst hurdle rates vary between banks and alternative funds, the cost of debt ranges from upper single digit up to mid double-digit IRRs with, in some instance, a minimum multiple on money requirement.

Fig. 1: Margins – Senior investment loans and development loans – Q1 2023

Source: Q1 2023 DC Advisory UK Real Estate Lender Survey

In addition to adjusting real estate and healthcare real assets debt lending markets, there has been considerable movement on the real estate and healthcare real assets bond market. Based on our observations and analysis, we believe notable pricing drops combined with upcoming maturities are triggering situations where creativity and innovation are key to unlock value and avoid dead-ends.

Conclusion

In short, debt has certainly become more expensive, reaching pre-crisis equity return levels[ix]. To balance out the risk/return profile, we believe that real estate valuations will inevitably come under further pressure, and so will debt covenants. Sponsors and creditors will need the right advice to navigate this new reality and avoid unnecessary collisions.

When the interest rate cycle turns, we would expect private equity funds to reduce debt exposure in favour of equity again.

Get in touch with DC Advisory’s dedicated UK Real Estate and Healthcare team that specialises in M&A, Capital Raising, Debt Advisory and Restructuring.

For important information about our insights and publications read our full disclaimer >

Sources

[i] The Advisor Channel, Dec 2021: Ranked: Real Estate Return on Investment by Sector (2012-2021) (visualcapitalist.com)

[ii] Axios, Aug 2022: Direct lending markets helps keep private equity deals flowing (axios.com)

[iii] The Q1 2023 DC Advisory UK Real Estate Lender Survey - DC Advisory’s independent survey of 30 direct lenders in the UK real estate market, which was completed in March 2023 and conducted across the UK (referred to herein as the “Q1 2023 DC Advisory UK Real Estate Lender Survey” or the “Survey”). Any data sourced from the Survey is limited to the data provided by the Survey participants and is not meant to constitute definitive market data. The lenders selected for the Survey are based on those that are most active in the market, and that DC Advisory interacts with the most. Accordingly, the Survey participants do not constitute an exhaustive list of lenders who may have been active during the period addressed by the Survey

[iv] Private Debt Investor, Feb 2023: Why LPs are taking a leap of faith (privatedebtinvestor.com)

[v] Private Debt Investor, Nov 2022: Investor appetite is changing as private debt matures as an asset class (privatedebtinvestor.com)

[vi] Q1 2023 DC Advisory UK Real Estate Lender Survey

[vii] GOLDEN SHARE | English meaning - Cambridge Dictionary

[viii] Investment Property Forum [Changing Sources of Real Estate Debt Capital: Facts and Implications], May 2017: b9981f32-104a-4a13-98494859bff40868.pdf (ipf.org.uk)

[ix] Q1 2023 DC Advisory UK Real Estate Lender Survey

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.