DC Discusses: The truth bearer role of the Chair

Date

5 min read

DC Advisory UK CEO, Tim Morris, recently shared his outlook on the market and insights on the role of the Chair as a truth bearer at our annual Chairs’ event, bringing together around 50 Chairs from across multiple industries, in partnership with PepTalks, Jamieson Corporate Finance, EtonBridge Partners & Stonehage Fleming. Key highlights include:

Despite market expectations of increasing M&A activity, there remains a lack of alignment between buyers and sellers, making it another challenging year for exits. This year so far, the European exit market has been weaker than 2023 – with an approximately 11% decrease in deal volume YoY.[1] Additionally, in 2024 so far, 84% of deals completed in Europe have been trade led, albeit 16% of those have been PE backed trade.[2]

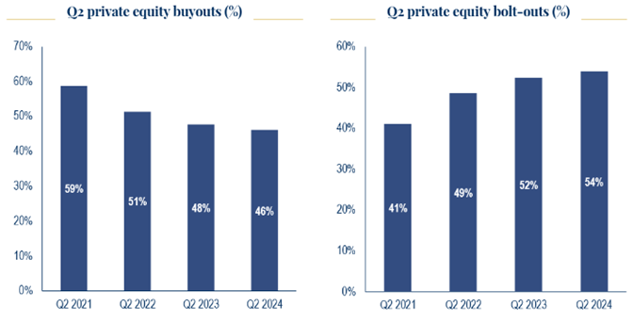

Whilst we have noted the expectation gap between buyer and seller has continued this year, and despite the wall of dry powder, this uncertainty has led to a further reduction in mid cap buyout transactions. At the same time, the trend for bolt-ons has continued to grow as a means to deploy capital, as we are aware that most investors now have buy-and-build thesis investments in their portfolios. This push-and-pull is demonstrated below, as the ratio of transactions representing private equity buyouts and bolt-ons have swapped over the past four years. Whereas buyouts made up most of the transactions in Q2 2021 (59%) and bolt-ons the minority (41%); we saw bolt-ons make up the majority in Q2 2024 (54%) and buyouts less than half (46%)[3]. Although we believe this is beneficial from a deployment perspective, there may be challenges on exit as the question of successful integration is not easy to answer, yet key to delivery.

Source: Mergermarket, Completed date, Europe only, deals with value between GBP 75 – 500M, undisclosed deal values included, private equity exits discounted from totals

Current market conditions are, in our view, seeing more sellers than buyers, due to private equity firms needing to provide liquidity to their LPs. Buyers are selective, seeking high-quality assets and willing to pass on lesser opportunities. We see exit routes are now including traditional trade buyers, private equity-backed buyers, and increasingly, secondary sales, with no return of IPO’s in 2024.

Continuation funds are increasingly used to generate exits, making up nearly half of GP led Secondaries volume in 2024 so far, marking another year increased volume[4]. The global continuation fund transaction volume reached $46bn in 2023, and numbers are set to exceed this for 2024[5].

Secondary sales offer liquidity options for private equity but also serve as an opportunity for management to extend their involvement and reset their approach for growth. Continuation funds made up around 80%, or $14.4bn, of total sponsor backed exit volume in H1 2023 – an almost 50% increase on the H1 2019 figure.[6]

The role of the Chair has evolved in recent years, becoming not only a mentor and coach, but a ‘truth bearer’ for management, advisors, and investors. Where perspectives of value from private equity backers or advisors may be overly optimistic, it is crucial that the Chair push for transparency and truth, so decisions can be informed by realistic assessments. Too many elongated or failed processes are a consequence of exploring an exit based on a lack of understanding of the sponsor ‘threshold price’ to trade, which the Chair is in a unique place to be able to ascertain and challenge themselves and advisors, if the business is in shape to exceed.

We believe the most successful businesses will show adaptability, agility, and resilience, all of which will become the wheelhouse of successful future Chairs. Across sectors, we have observed that a ‘successful’ Chair is the truth bearer able to help management, sponsors and advisors to ensure alignment and a successful exit.

As we enter the final quarter of the year, debt markets have strengthened considerably, despite continued geopolitical uncertainty, we believe the strength of the debt markets, a lowering interest rate trajectory and lower inflation will provide a stronger market for exits to unlock the wall of PE dry powder in Q4 and 2025. We see the ‘truth bearer’ playing a key role in continuing the expected increase in general and PE transaction activity.

If would like to discuss any of the themes discussed in more detail, please get in touch with Tim Morris here >

Register interest for future Chairs’ events here >

This article has been prepared solely for information purposes and is not intended to function as a “research report.” In particular, this means that it is not intended, nor does it contain sufficient information, to make a recommendation as to the advisability of investment in, or the value of, any security.

Any link or reference to a third-party website contained in this article does not constitute an endorsement of any third-party content published on such website.

Additionally, this article does not constitute or form part of, and should not be construed as, an offer to sell, or a solicitation of any offer to buy, or any recommendation with respect to, any securities. You should not base any investment decision on this article; any investment involves risks, including the risk of loss, and you should not invest without speaking to a financial advisor.

For additional important information regarding this article, please see insights and publications disclaimer.

References

[1] Mergermarket: Completed date, Europe only, deals with value between GBP 75 – 500M, undisclosed deal values included, private equity exits discounted from totals

[2] Mergermarket: Completed date, Europe only, deals with value between GBP 75 – 500M, undisclosed deal values included, private equity exits discounted from totals

[3] Mergermarket: Completed date, Europe only, deals with value between GBP 75 – 500M, undisclosed deal values included, private equity exits discounted from totals

[4] https://www.privateequityinternational.com/reinventing-continuation-funds/

[5] https://www.ipe.com/investment/private-credit-secondaries-come-of-age/10072985.article

[6] https://www.privateequityinternational.com/continuation-funds-continue-their-streak-story-of-the-year/

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.