DC Discusses: Why the auto aftermarket is revving up for 2024

Date

13 min read

DC Advisory attended the 55th annual Specialty Equipment Manufacturers Association (SEMA) and the 31st annual Automotive Aftermarket Expo (AAPEX) trade shows held in Las Vegas, NV October 31 through November 3. SEMA and AAPEX are the world’s preeminent automobile aftermarket trade events where manufacturers and service providers unveil their latest offerings to buyers, distributors and members of the press.

DC Advisory’s US Consumer, Leisure & Retail team discuss the future of the industry in more detail >

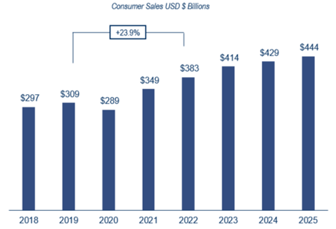

The $383 billion auto aftermarket – encompassing all manufacturing, retailing and servicing of a vehicle after it has been sold to the consumer – is expected to grow 8.1% in 2023 following last year’s outperformance of industry forecasts of 9.7% growth in 2022[1]. While overall industry sales posted record performance in 2022[2], sales for specialty-equipment manufacturers – which includes such categories as aftermarket performance and accessory parts – is projected to have slowed last year, growing only 2% to $51.8 billion[3]. This slowdown has been in large part driven by supply chain challenges impacting both new vehicle and aftermarket manufacturers, technological changes including electrification and autonomy, changes in consumer preference as a result of shifting work-from-home policies, waning pandemic-era savings and continued economic uncertainty impacting consumer purchasing behavior.

Despite these potential challenges, specialty equipment sales are expected to return to more typical growth of 3-4% annually in 2024 and beyond with the broader automotive aftermarket also expected to return to similar rates following strong 2023 performance [4].

Supported by strong industry fundamentals – including a growing and aging car parc, increasing vehicle usage as measured by vehicle miles travelled and a core enthusiast customer base – we believe that the auto aftermarket industry will continue to represent an attractive M&A opportunity for both private equity and strategic parties.

US Automotive Aftermarket Growth: [5]

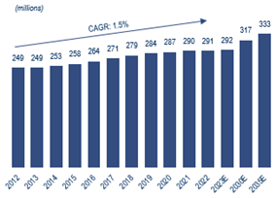

While there are numerous factors impacting the automotive aftermarket, the strongest indicators of long-term aftermarket spend have historically been miles driven, average age of vehicles on the road and the size of the car parc.

Of the more than 290 million light vehicles in operation in the US[6], almost 122 million are over 12 years old, with the average age of cars and light trucks now a record 12.5 years (+12.6% since 2012) [7]. Similarly, usage of vehicles (and resultant wear-and-tear) as measured by vehicle miles travelled (VMT) has also increased. Total VMT for the last twelve months ending June 2023 was 3.2 trillion – registering ~1% growth from the 3.17 trillion recorded in June 2022, on top of the 4.2% growth from the previous year[8]. With more and more (aging cars) on the road – a 17% increase since 2013[9] – and increasing miles driven – the aftermarket industry can rely on macro factors continuing to provide opportunities for growth. In particular, we see categories that cater to an increase in vehicle age and usage – including aftermarket repair and maintenance, tire sales and replacement parts and accessories – being long-term winners over the next several years.

Average Vehicle Age [10]

Light Vehicles in Operation [11]

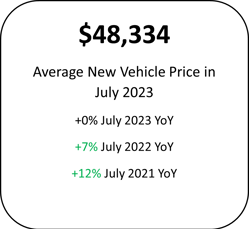

Following several years of challenges, most notably within semiconductors but pervasive across almost all parts categories, auto supply chains are progressing towards a meaningful recovery.[12] While analysts do not project new vehicle sales recovering to pre-pandemic levels over the forecast period, increased vehicle availability has alleviated some consumer and fleet pent-up demand, helping to fuel a significant YoY unit sales increase (+9%) with sales into rental and commercial fleets increasing notably, up roughly 60% and 40% YoY, respectively[13]. Additionally, September 2023 data indicates a total light vehicle SAAR* of 15.7 million, up 14.4% YoY, suggesting an acceleration in seasonally adjusted sales[14]. Inventories of unsold vehicles have increased to 2.21 million this month[15], a 60% increase YoY, which further suggests a recovery for the new car supply – although this increase in available vehicles, as well as SAAR in general, were likely negatively impacted by the UAW strikes [16]. Overall, from a consumer perspective, we are witnessing a slowdown in growth of new vehicle prices (+0% YoY in July 2023 vs. +7% in July 2022) and an even more pronounced correction in used vehicle prices (-6% YoY in July 2023 vs. -1% in July 2022)[17].

*Seasonally Adjusted Annualized Rate – used to track vehicle registration performance giving a better representation of automotive market activity

US New Light-Vehicle Sales Forecast [18]

US New Light-Vehicle Sales Forecast [18]

US New Vehicle Average Transaction Price in July 2023:[19]

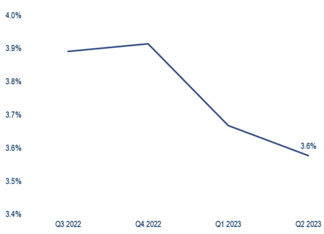

We are observing an evening distribution in sales between online and brick and mortar stores as inventories improve and consumers head back to physical retail stores. In the US[20] as is the case in Europe, brick and mortar growth outpaced digital in 2022 for the first time since tracking began in 2000[21] a clear swing from 2020 and 2021 where e-commerce consistently outpaced brick-and-mortar growth by a factor of 10[22]. Despite this recent normalization in growth, the US motor vehicle and parts e-commerce industry remains strong with a $69 billion valuation in 2022 and is anticipated to expand at a 13.8% CAGR over the next ten years[23].

US Motor Vehicle & Parts E-Commerce as a % of Total Store and Non-Store Sales[24]

While the automotive industry has proven resilient on the whole, we have observed that more discretionary categories such as performance parts and accessories have been hit harder in the current environment. Anecdotally, many manufacturers have experienced a slowdown in demand as enthusiasts delay purchases or opt for cheaper alternatives during times of budgeting[25]. We believe that given the enthusiast nature of these products, this downturn is not reflective of a broader shift in consumption but an episodic dip as a result of macroeconomic pressures. Less discretionary categories such as tires, brakes and routine maintenance products are also being impacted by trading down and maintenance deferrals, although this downward impact is limited given the fairly inelastic demand for these types of mission-critical products[26].

The popularity of electric vehicles and other new technologies has continued to grow significantly in recent years, with electric vehicle sales now representing 7% of the new vehicle market in Q1 2023 – more than four times its 2020 level[27]. Adoption of electric mobility, especially among younger consumers and those with higher household income, is projected to grow in the double-digits through 2028[28]. While there have been material improvements over the last 5 years, the most significant barriers preventing consumers purchasing electric vehicles remain charging infrastructure and related range anxiety. As of Q1 2023 there were over 160,000 public charging points in the US, more than double the Q4 2019 pre-pandemic level [29], with the network set to benefit from increased federal investment including over $7.5 billion earmarked for the construction of 500,000 charging points as part of 2021’s Infrastructure Investment and Jobs Act [30]. We have observed thriving investments in manufacturing over the past eight years in tooling up for EV production – $120 billion[31] – indicating that manufacturers are planning for a substantial increase in demand for battery electric vehicles. And while some industry participants are noting a recent slowdown in electric vehicle sales[32], in the long-term, electric and hybrid vehicles are likely to continue displacing traditional internal combustion engines. We believe that both financial sponsors and strategic parties will be focusing intently on understanding the purchase behaviors of the new EV consumer with respect to the automotive aftermarket – e.g., the frequency of updating accessories, personalizing vehicles, pursuing performance upgrades as well as aftermarket charging equipment – in order to determine where to target in the space. This year’s SEMA Show featured an expanded SEMA Future-Tech studio section that included the latest advancements in battery electric, hybrid and fuel cell vehicle technology, an expansion from 2021 and 2022 and consistent with overall industry trends.

Within the aftermarket industry, companies are seeing continued opportunity in the off-road, overlanding, performance upgrades and classic vehicles spaces, among others. Pickups represent one of the largest classes of vehicles in the US with more than 50 million vehicles on the road [33] and are commonly accessorized for off-road applications with 62% of pickup owners buying off-road parts [34] or taking their vehicles off-road and a similar percentage (49%) making application-specific add-on purchases [35] – from toolboxes and storage to suspension and towing upgrades to performance and oversized tires to caps and tonneau covers.

The pickup category represented approximately $16 billion in specialty equipment sales in 2022, with about $4 billion consisting of truck caps, covers, racks and other accessories[36]. Similarly, we are seeing increased popularity for overlanding and “van lifestyle” activities, which combines remote travel, off-roading and camping. This category overall has benefited from a meaningful increase in outdoor recreation participation since the pandemic (+ 9.2%) with a large influx of younger and more affluent consumers[37]. Roof racks, rooftop tents and related accessories continue to represent an intriguing opportunity for sector acquirers.

There is additional opportunity in the performance upgrade space with a $3.1 billion specialty equipment sports car market size and sports cars being some of the most accessorized and enthusiast-owned vehicles[38]. Classic vehicles also remain attractive enthusiast platforms for modification, upgrades and restoration with around 12 million pre-1990 classics currently in the US and the industry generating roughly $2.4 billion in annual sales.[39] This category has long benefited from a “nostalgia factor” but has recently experienced a significant uptick in demand from millennial customers, with “restomods” (restored vehicles with modern amenities) and vintage SUVs like Ford Broncos and Toyota Land Cruisers increasingly being coveted by younger consumers[40]. This year's SEMA Show featured numerous classic EV Conversions, including a stunning mid-80's Porsche 911 Carrera.

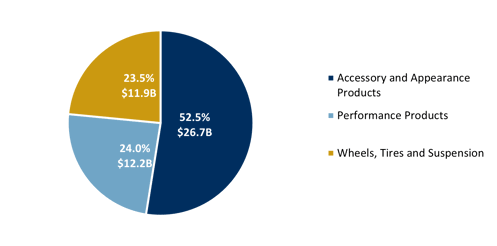

2022 Specialty Equipment Spend Breakdown[41]

Though M&A activity has so far this year lagged 2022 levels, we are optimistic that a recovery is on the horizon. Q2 2023 deal volume decreased 8% from Q1 2023 and 29% from Q2 2022, a marketed decline from the robust M&A markets of 2021[42]. Despite this, deal volumes will likely begin to increase in 2024 as the automotive industry continues its upward trend toward pre-pandemic performance levels, and industry participants continue to prepare for an electric future[43]. We believe that M&A interest in the sector will increase as the aforementioned strength in macro industry trends combined with improvements in the economy drive consumer demand within the category. And as transaction volume returns to historical levels, we suspect this will result in healthy opportunities for strategic and financial acquirers to deploy capital as well as owners to sell businesses.

To discuss any of the themes explored in this article, get in touch with the Consumer, Leisure & Retail team here >

This article has been prepared solely for information purposes and is not intended to function as a “research report.” In particular, this means that it is not intended, nor does it contain sufficient information, to make a recommendation as to the advisability of investment in, or the value of, any security.

Additionally, this article does not constitute or form part of, and should not be construed as, an offer to sell, or a solicitation of any offer to buy, or any recommendation with respect to, any securities. You should not base any investment decision on this article; any investment involves risks, including the risk of loss, and you should not invest without speaking to a financial advisor.

For additional important information regarding this article, please see insights and publications disclaimer.

References

[1] Aftermarket Matters, ‘Automotive aftermarket industry analysis — 2023’, September ’23 https://www.aftermarketmatters.com/national-news/automotive-aftermarket-industry-analysis-2023/

[2] Aftermarket Matters, ‘Automotive aftermarket industry analysis — 2023’, September ’23 https://www.aftermarketmatters.com/national-news/automotive-aftermarket-industry-analysis-2023/

[3] SEMA, ‘2022 SEMA Market Report’, June ’22 https://sites.sema.org/market-research/pdf/100019_SEMA_Market_Report_2022.pdf

[4] PR Newswire, ‘Auto Care Industry Expected to Grow 8.1% in 2023’, June ’23 https://www.prnewswire.com/news-releases/new-research-auto-care-industry-expected-to-grow-8-1-in-2023--reach-574-billion-in-2026--301851936.html

[5] SEMA, ‘2022 SEMA Market Report’, June ’22 https://sites.sema.org/market-research/pdf/100019_SEMA_Market_Report_2022.pdf

[6] Hedges & Company, ‘US vehicle registration statistics’, August ’23 https://hedgescompany.com/automotive-market-research-statistics/auto-mailing-lists-and-marketing/

[7] S&P Global, ‘Average Age of Light Vehicles in the US Hits Record High 12.5 years’, May ’23 https://www.spglobal.com/mobility/en/research-analysis/average-age-of-light-vehicles-in-the-us-hits-record-high.html

[8] St. Louis Fed, ‘Vehicle Miles Traveled’, September ’23 https://fred.stlouisfed.org/series/TRFVOLUSM227NFWA

[9] Hedges & Company, ‘US vehicle registration statistics’, August ’23 https://hedgescompany.com/automotive-market-research-statistics/auto-mailing-lists-and-marketing/

[10] SEMA, ‘2022 SEMA Market Report’, June ’22 https://sites.sema.org/market-research/pdf/100019_SEMA_Market_Report_2022.pdf

[11] SEMA, ‘2022 SEMA Market Report’, June ’22 https://sites.sema.org/market-research/pdf/100019_SEMA_Market_Report_2022.pdf

[12]Bloomberg, ‘Car Prices Are Starting to Ease as Pandemic Supply-Chain Issues Fade’, June ’23 https://www.bloomberg.com/news/articles/2023-06-30/car-prices-are-starting-to-ease-as-pandemic-supply-chain-issues-fade

[13] Cox Automotive, ‘New-Vehicle Market Shrugs Off High Loan Rates, UAW Strike, Closes Q3 on a Strong Note; September Sales Forecast by Cox Automotive to be Up 13% Year Over Year’, September ’23 https://www.coxautoinc.com/news/cox-automotive-forecast-september-2023-u-s-auto-sales-forecast/

[14] NADA Market Beat, ‘13th Straight Month of Year-over-Year New Light-Vehicle Sales Increases’, September ’23 https://www.nada.org/nada/nada-headlines/nada-market-beat-13th-straight-month-year-over-year-new-light-vehicle-sales

[15] Cox Automotive, ‘New-Vehicle Inventory Rises Despite UAW Strike; GM Most Vulnerable’, October ’23 https://www.coxautoinc.com/market-insights/new-vehicle-inventory-september-2023/

[16] NADA Market Beat, ‘13th Straight Month of Year-over-Year New Light-Vehicle Sales Increases’, September ’23 https://www.nada.org/nada/nada-headlines/nada-market-beat-13th-straight-month-year-over-year-new-light-vehicle-sales

[17] Cox Automotive, Used-Vehicle Supply Drops on Strong Sales, September ’23 https://www.coxautoinc.com/market-insights/used-vehicle-inventory-august-2023/

[18] SEMA, ‘2023 SEMA Market Report’, October ‘23 https://sites.sema.org/market-research/

[19] Cox Automotive, ‘Kelley Blue Book Analysis: New-Vehicle Transaction Prices Up Less Than 1% Year Over year, Smallest Increase in Decade’, August ’23 https://www.coxautoinc.com/market-insights/kbb-atp-july-2023/

[20] St. Louis Fed, ‘Motor Vehicle and Parts E-Commerce Sales’, June ’23 https://fred.stlouisfed.org/series/ECOMSA

[21] Econsultancy, ‘How hybrid shopping trends are impacting automotive retail’, April ’23 https://econsultancy.com/multichannel-automotive-retail-trends/

[22] Cox Automotive, ‘Transformation Toward eCommerce in Automotive Retailing’, December ’21 https://www.coxautoinc.com/market-insights/transformation-toward-ecommerce-in-automotive-retailing/

[23] Global Market Insights, ‘E-Commerce Automotive Aftermarket’, May ‘23 https://www.gminsights.com/industry-analysis/e-commerce-automotive-aftermarket

[24] Retail Indicators Branch – US Census Bureau, ‘Quarterly Retail E-Commerce Sales’, August ’23 https://www.census.gov/retail/ecommerce.html

[25] Holley Investor Presentation, May ’23 https://investor.holley.com/events-and-presentations/presentations/presentation-details/2023/Investor-Presentation---May-2023/default.aspx

[26] Modern Tire Dealer, “Monro CEO Is Hopeful Consumers Are Ready to Spend Again”, October ’22 https://www.moderntiredealer.com/retail/article/11461226/monro-ceo-is-hopeful-consumers-are-ready-to-spend-again

[27] Clean Technica, ‘US Electric Vehicle Sales Up 66%, Rise To 7% Of US Auto Sales’, April ’23 https://cleantechnica.com/2023/04/27/us-electric-vehicle-sales-up-66-in-1st-quarter/

[28] Hedges & Company, ‘Demographics of car buyers’, January ’19 https://hedgescompany.com/blog/2019/01/new-car-buyer-demographics-2019/#ev_owner_demographics

[29] Office of Energy Efficiency & Renewable Energy, ‘The Number of Electric Vehicle Charging Ports in the U.S. Nearly Doubled in the Past Three Years’, July ’23 https://www.energy.gov/eere/vehicles/articles/fotw-1299-july-17-2023-number-electric-vehicle-charging-ports-us-nearly

[30] The White House, ‘Fact Sheet: The Bipartisan Infrastructure Deal’, November ’21 https://www.whitehouse.gov/briefing-room/statements-releases/2021/11/06/fact-sheet-the-bipartisan-infrastructure-deal/

[31] Environmental Defense Fund, “Report Finds Investments in U.S. Electric Vehicle Manufacturing Reach $120 Billion, Create 143,000 New Jobs”, March ’23 https://www.edf.org/media/report-finds-investments-us-electric-vehicle-manufacturing-reach-120-billion-create-143000

[32] Reuters, ‘More alarm bells sound on slowing demand for electric vehicles’, October ’23 https://www.reuters.com/business/autos-transportation/more-alarm-bells-sound-slowing-demand-electric-vehicles-2023-10-25/

[33] Truck Hero S-1 Registration Statement, https://www.sec.gov/Archives/edgar/data/1648189/000119312515346140/d17828ds1.htm

[34] SEMA, ‘2023 SEMA Market Report’, October ‘23 https://sites.sema.org/market-research/

[35] SEMA, ‘SEMA Pickup Accessorization Report Offers Comprehensive View of Truck Landscape’, https://www.sema.org/news-media/enews/2022/48/sema-pickup-accessorization-report-offers-comprehensive-view truck#:~:text=We%20see%20a%20lot%20of,those%20who%20accessorize%20(49%25)

[36] SEMA, ‘2022 SEMA Market Report’, June ’22 https://sites.sema.org/market-research/pdf/100019_SEMA_Market_Report_2022.pdf

[37] Outdoor Industry Association, ‘2023 Outdoor Participation Trends Report’, https://www.sema.org/news-media/magazine/2021/12/rise-overlanders

[38] Clean Technica, ‘US Electric Vehicle Sales Up 66%, Rise To 7% Of US Auto Sales’, April ’23 https://cleantechnica.com/2023/04/27/us-electric-vehicle-sales-up-66-in-1st-quarter/

[39] SEMA, ‘2023 SEMA Market Report’, October ‘23’ https://sites.sema.org/market-research/

[40] Forbes, ‘Millennials Take The Wheel Of Vintage Car Collecting, And It’s A Fun Ride’, June ’20 https://www.forbes.com/wheels/features/millennials-vintage-car-collecting/

[41] SEMA, ‘2022 SEMA Market Report’, June ‘22’ https://sites.sema.org/market-research/pdf/100019_SEMA_Market_Report_2022.pdf

[42] JustAuto, ‘M&A in automotive decreased in Q2 2023’, July ’23 https://www.just-auto.com/deals-dashboards/global-ma-activity-automotive-industry/

[43] PWC ‘Auto M&A cools — yet showing healthy activity’ June ’23 https://www.pwc.com/us/en/industries/industrial-products/library/automotive-deals-outlook.html

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.