Consumer, Leisure & Retail saw significantly higher transaction volumes in H1 2021 (c.110% increase compared to H1 2020)[1], driven by the recovery in consumer spending

That said, the key growth area within the vertical in 2020 was consumer internet, which accounted for 90% of the Consumer, Leisure & Retail deals completed[2]

Consumer and business ecosystems have changed due to the pandemic – ie the substitution of offline touchpoints with online ones and disruption in global supply chains – both of which have led to an increase in organized retail and the proliferation of direct-to-consumer (D2C) models. This is apparent from the investments that have been made in:

D2C start-ups across all categories, such as personal care (eg Sugar Cosmetics, WOW Skin Science, Purplle, MyGlamm), online grocery providers (Tender Cuts), and automobile ecommerce (CarTrade, GoMechanic)[3]

Thrasio-style start-ups, such as Global Bees (FirstCry)[4], Mensa Brands[5], and GOAT Brand Labs[6], which have raised funds without any significant operations, as they aim to scale up-and-coming D2C brands with their marketing, technological and operations expertise

Online gaming platforms received large-size investments in H1 2021 (Dream11, Mobile Premier League, WinZO)[7], as the pandemic drove a spike in online gamers due to lockdown, which has been well maintained despite restrictions easing. We expect this to increase as start-ups continue to demonstrate user stickiness and esports emerges as a viable career alternative

Increasing digital penetration in tier-2 and tier-3 cities in India[8] led to higher investments in content and social media apps, especially those allowing communication in vernacular languages (for example, Dailyhunt[9], Koo[10] and ShareChat[11]). We expect this to continue given the ban imposed on a host of Chinese apps [12] and see an increase in the number of Indian social media platforms to cater to this void

Food delivery platform Zomato is expected to float its IPO in H2 2021[13] and will be one of the first tech start-ups to go public in India since Info Edge in 2006. The reception from public markets will determine the IPO path for many other tech unicorns looking to provide an exit to its investors via listing. Successful IPO exits will further provide incentives for investments in the consumer internet space

As this new digital consumer ecosystem continues to evolve, we expect e-commerce businesses - both horizontal and vertical, across categories such as personal care, food & beverages, lifestyle etc, and those with B2B business models that enable merchants to move online - to receive increased interest from investors. However, a slower recovery in offline discretionary spend is expected as public gatherings continue to be restricted and a decent level of vaccination is required for malls, cinema theatres etc to fully open up

Source: Venture Intelligence Private Equity & Venture Capital Deals Database[14]

Financial Services

Financial services saw as many transactions in H1 2021 as in the whole of 2020[15], caused by a surge in digital payments (due to lockdowns), insurtech (increased health consciousness, simplification of traditional processes) and personal finance (wealth management)

Fintech has, so far, witnessed strong traction in terms of deal value with 6 companies attaining unicorn status in the first half of 2021 out of the 15 overall[16]

While interest spanned all sub-sectors, payments remained the main beneficiary of interest in the India fintech market, in spite of a drop in offline payment volumes due to national lockdowns. Companies enabling payments are seen as the first step in the digitization journey and will continue to be in focus

Optimism and conviction is evident in a highly uncertain cryptocurrency market in India, demonstrated by the funding received by CoinSwitch from Tiger Global[17]. We expect investments in this sub-sector to increase over the next few years once there is more regulatory certainty around cryptocurrencies

The second wave of the pandemic and the second moratorium announced by RBI[18] has added to existing concerns around non-performing assets (NPAs). As a result, funding in both traditional and digital lenders have trailed the broader market and will continue to remain muted in the medium term

Source: Venture Intelligence Private Equity & Venture Capital Deals Database[19]

Healthcare

Healthcare witnessed an increase in deal volumes in H1 2021 (+33% compared to H1 2020[20]), recovering from 2020 as uncertainty over the pandemic’s impact subsided

The recovery in hospital occupancy, which witnessed a huge fall in H1 2020 due to reduction in elective procedures and increased clarity on the supply chain in the pharma sector, has led to an almost doubling in deal value ($2.3bn in H1 2021 vs $1.4bn in H1 2020)[21] with multiple large-size, late-stage and buyout deals

For example, the buyout of Zydus Cadila’s animal health business by Multiples for $398m[22], and investments into Manipal Hospitals by TPG Capital, Temasek and NIIF amounting to $435m[23]

Pharmaceuticals continues to drive deals in the sector with two-thirds of completed Healthcare transactions in H1 2021 in this segment[24]. While the traditional pharma sector (API, domestic formulations) is relatively resilient and defensive, sizeable investments are being made in upcoming sectors[25], such as biosimilars, gene bioinformatics, genetics etc, as India tries to move up the value chain from being an outsourcing hub to an R&D hub. We expect buyouts in this space to reduce and growth investments to increase given favourable policies from the Indian government to encourage domestic production[26]

Reduced deal activity in 2020 has spurred momentum in 2021. Sizeable assets, such as Manipal Hospitals, innovative business models like Pristyn Care, and healthtech companies, have been garnering attention[27]. The emergence of the second wave of Covid-19 led to a fall in occupancy again for hospitals, but deal activity has subsisted. We expect increased transactions in the space, however, with minor contraction in valuations

Source: Venture Intelligence Private Equity & Venture Capital Deals Database[28]

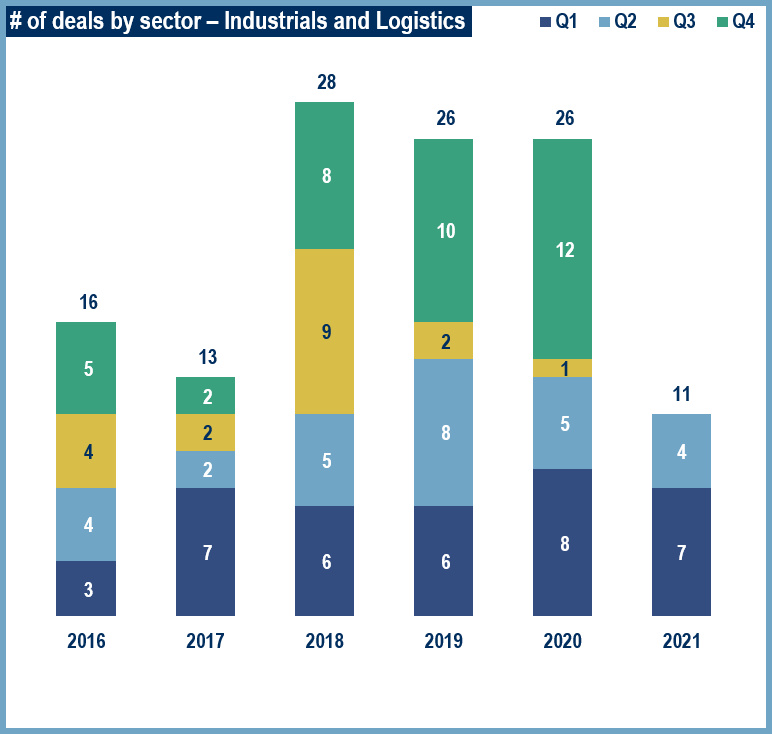

Industrials and Logistics

Industrials and Logistics witnessed similar activity in H1 2021 compared to 2020[29]

Buoyancy in capital markets has led to companies with sizeable EBITDA opting for the IPO route to raise capital, and provide exit opportunities to their investors. The speciality chemicals sector is a good example where many companies such as Laxmi Organic[30], Anupam Rasayan[31], and India Pesticides[32] all opted for IPOs

Newer B2B e-commerce platforms, such as Moglix and Infra.Market[33] (both of which attained unicorn status this year), are aggregating fragmented demand and supply channels while adding the convenience of digital ordering, improving the existing supply chain and saving cost through economies of scale. We expect this trend to increase as there are huge inefficiencies in the manufacturing sector, providing large market opportunities

Unlike H1 2020, logistics transactions in 2021 were geared more towards tech logistics, as they aim to disrupt various stages of supply chains, from the factories to the end users - companies such as Delhivery and Elastic Run are prime examples of this[34]. This is expected to continue as more companies in this sector focus on profitability and capital efficiency - an area of concern for investors

We believe that financial sponsors have a renewed appetite for large buyout transactions across Industrials’ sub-sectors, especially in packaging and logistics, driven by expected economic recovery and improvement of the overall supply chain ecosystem in India

Source: Venture Intelligence Private Equity & Venture Capital Deals Database[35]

IT, ITeS & SaaS

The deals in IT, information technology-enabled services (ITeS) and software as a service (SaaS) picked up pace in H1 2021 (30 vs 15 in H1 2020)[36]. 2020 transactions were undoubtedly impacted by pandemic uncertainty, and for those companies catering to specific sectors (eg financial services), the pandemic’s impact on their end clients

Riding the pandemic tailwinds, the Indian SaaS market witnessed three start-ups joining the unicorn club in H1 2021[37] and we believe at least two others are slated to turn into unicorns by the end of the year

Aggressive cloud adoption across the globe is expected to expand addressable markets for category leaders in emerging tech

Indian SaaS companies continue to win market share in the US and UK markets and command premium valuations on account of a strong focus on emerging use cases, eg API, data analytics etc, India-based cost arbitrage and a large IT talent pool

With enterprises in Asia migrating to cloud at a much faster pace than their US counterparts[38], companies also focussing on the highly underpenetrated markets of Southeast Asia and the Middle-East are expected to gain strong investor interest

The IT services market continues to be a key beneficiary of the Covid-induced digitization drive. Private equity interest, especially in the buyout space, continues to remain high with transactions such as Acolyte Digital’s strategic partnership with New Mountain Capital[39] and Sverica Capital Management’s investment in WinWire Technologies[40]

Additionally, accelerated cloud adoption and working from home has driven increased transactions in cybersecurity, such as the 1Kosmos funding transaction that was completed in February 2021[41]. This is expected to gather steam due to an increased number of data breaches[42]

Source: Venture Intelligence Private Equity & Venture Capital Deals Database[43]

Services

Within Services, EdTech continued to be the most active sub-sector due to the sustained growth of online learning and schools reopening at a slower pace. However, mid-market private equity activity in the EdTech space slowed down in H1 2021 ($0.6b deal value against $1b in H1 2020)[44], driven by competing aggressive consolidation, led by Byju’s[45], Unacademy[46] and Upgrad[47]

The scaled-up players, who traditionally operated in either K12, test preparation or professional learning sectors, are now widening their scope through acquisitions to capture value across the student lifecycle

Byju’s (K12) acquisition of Aakash Education (test preparation)[48], and Upgrad’s (professional training) acquisition of The Gate Academy (test preparation)[49] are testaments to this

Financial sponsor interest is expected to be robust over the next couple of quarters for companies operating in the niche sub-sectors with strong business moats; recent examples include the funding rounds in LEAD School (B2B K12)[50], Classplus (K12 tutoring SaaS)[51] and Playshifu (STEM toys for kids)[52]

Source: Venture Intelligence Private Equity & Venture Capital Deals Database[50]

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists: