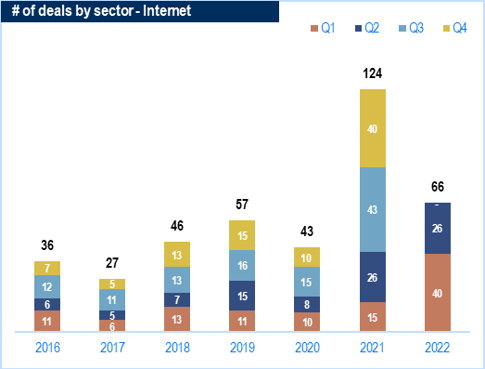

Consumer Internet & Digital

- Despite the reopening of offline sales, consumers continued to show preference for the convenience of online channels, leading to sustained growth in the space both for new age and traditional players. The internet sector has seen 66 transactions in H1 2022 (vs 41 in H1 2021) – although deal value remained level at c.USD 4.5BN, with mid-market deals in this space accounting for a third of total transaction volumes and value [1]. As new business models emerge to cater to evolving customer needs, platforms and aggregators continue to show strong performance in H1 2022:

- D2C Brands showed robust traction in H1 2022, with brands in the cosmetics, personal care, apparels and accessories segments receiving investor’s attention.[2] We have witnessed these companies display the ability to create a direct connection with consumers, by leveraging the right mix of marketing, targeting, and pricing. With consumers demanding more convenience from online services, platforms like Zepto, Dunzo and Blinkit have raised mega funding rounds.[3] We expect to see some rationalisation in this space as investors chase elusive positive unit economics in this high-burn sector.

- Continuing the trend from the previous year, roll-up start-ups continue to attract funding as this sector matures with Thrasio entering Indian markets.[4] This entrance of a global incumbent illustrates the scale of the opportunity that exists in the country. Given the continued confidence in this business model and potential for these companies to raise additional funding through debt, we expect to see adequate exit opportunities for mid-sized D2C brands

- Investments in content and gaming continued its momentum in H1 2022, with increased interest in sports and related content[5]. Companies including Rario[6] and Fancraze[7] in the NFT domain focused on sports, while livestreaming platforms like Loco[8] raised substantial funding as they provide new and unique avenues for customer engagement. We believe that companies in this space will continue to attract funding, as India sees a push from a combination of low-cost internet data and smartphones as well as a growing base of gamers[9]

- Overall, while we expect sustained deal activity in this sector, we believe investors will re-base their valuation expectations in the near future as companies attempt to prove the robustness of their business models, and nascent sectors such as gaming, agri-tech and D2C brands will likely continue to see traction

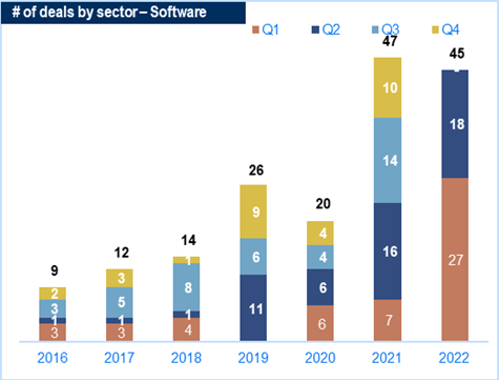

SaaS (Software-as-a-Service)

- The Indian SaaS sector has seen phenomenal deal volumes for H1 2022 (45 deals) almost matching the entire 2021 deal count (47 deals) [11] Overall transaction value in H1 2022 was c.91% higher than in H1 2021 at USD 2.7BN[12]. Increasing digitization across industries, higher cloud adoption, business process automation, amongst others, have been key growth levers for the sector

- Five of the 18 new unicorns in H1 2022 belong to the SaaS category, the most in for any sector so far and matching the total tally of new SaaS unicorns in 2021[13] - including Leadsquared (Salestech)[14], Hasura (Programming Tools)[15], and Uniphore Software (Conversational AI)[16]

- Indian SaaS start-ups are investing in expanding their presence heavily in global markets with North America and Europe presenting attractive market opportunities for most companies.[17] Companies like Postman, MoEngage and Whatfix are competing with entrenched incumbents in their own backyard, while others like Darwinbox continue to operate in the underserved domestic market with superior and differentiated offerings

- Globally, SaaS multiples have seen a significant decline, depleting by ~40% of last year’s numbers.[18] The ‘growth at all costs’ mindset is a thing of the past, as financial sponsors look for strong balance sheets, profitable unit economics, and high-growth expectations. We expect India will continue to deliver on its sustainable competitive advantage of an abundant digitally skilled workforce and low-cost structure, but SaaS will likely see more subdued deal activity in the country for the next two quarters.

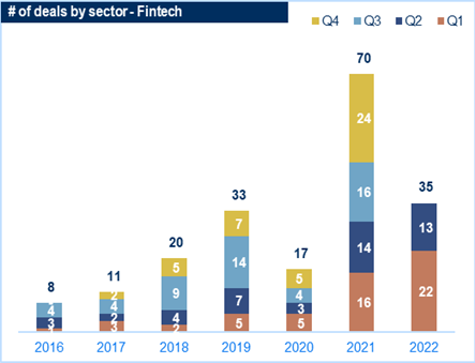

Fintech

- Fintech is the third largest beneficiary of the rising adoption of internet in the country, accounting for 17.4% of total transactions in H1 2022[20]. The sector continues to see momentum post-covid with a marginal increase in number of deals at 34 (a c.17% increase) and deal value at USD 2.4 BN, a c.16% increase vs H1 2021.[21] This was driven, in our view, by continued confidence in lending, buoyed by demand for new age lending platforms to cater to digitally savvy individuals and businesses

- H1 2022 saw the rise of four new fintech unicorns in credit (Oxyzo & CredAvenue), Neo banking (Open) and Web3 Infrastructure (Polygon, bringing the tally of fintech unicorns to 22 (of 103 total).[22] We expect to see continued enthusiasm for sub-sectors across fintech, particularly those focused on rapid digitization and inclusion, for MSMEs in the coming quarters

- While there is keen interest in all sub-sectors of fintech, lending remains the favourite of investors (c.37% of total fintech transactions vs c.17% for wealth-tech).[23] Going forward, we expect to see a slowdown in this sector, as non-banking lending companies feel the effect of rising interest rates[24]. Additionally, the Reserve Bank of India’s recent circular limiting capabilities of certain BNPL players taking advantage of regulatory arbitrage is likely to give pause to investor sentiment.[25] However, comprehensive lending platforms (one-third of total funding rounds in the lending sub-segment)[26] like Oxyzo & CredAvenue will likely remain in focus as they deliver value to both the underbanked 63-million-unit strong MSME segment,[27] as well as investors looking for alternative lending products

- The imposition of heavy taxes on cryptocurrency gains and withdrawal of banking support via the Unified Payments Interface (UPI) has negatively impacted cryptocurrency exchanges.[28] We believe that while the cryptocurrency space will see muted investor interest, early indications in the Web3 space based on sub-USD 10M transactions[29] suggest a potential uptick in the middle market going forward

- We expect that while global market conditions will likely bring a pause to investments in the mid-market space, fintech will remain a sector of choice in India in the coming quarters

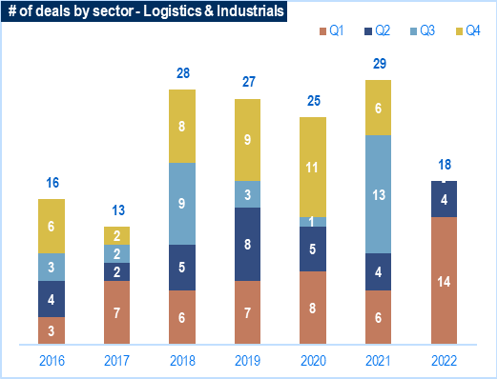

Industrials and Logistics-Tech

- Industrials & Logistics witnessed a c.111% increase in deal value to USD 2.5BN, combined with an 80% increase in volumes to 18 deals in H1 2022 over USD 1.16BN and 10 deals respectively in H1 2021[31]

- This growth is driven primarily by the buoyancy in the tech-logistics sector (c.43% of total deal value) with players such as ElasticRun and XpressBees each raising significant growth investments in excess of USD 300M[32] to enter the unicorn club[33]

- Given that tech logistics players are bringing transparency and efficiency to the traditional logistics space, there is likely to be continued investor interest in this space going forward

- Several highly profitable companies in the industrials segment including Aether Industries (Specialty chemicals)[34] and Venus Pipes & Tubes (Metals)[35] underwent their IPO debuts despite flagging investors’ confidence in the capital markets. We expect players with strong fundamentals to attract investor attention in the coming quarters

- As global OEMs commit to adoption of EV technology, this sub-sector continues to capture the interest of investors. Ola Electric[36] and Ather Energy[37] have raised significant rounds to expand their manufacturing capabilities and charging infrastructure as well as focus on R&D for new products. Electric commercial vehicles are also seeing a breakout in funding this year with Altigreen Propulsion[38] and EVage Ventures[39] raising funding in H1 2022

- Rising fuel prices and domestic oil imports[40] are likely to result in above average interest in the electric mobility space, though the ongoing chip shortage may temper demand in the near term[41]

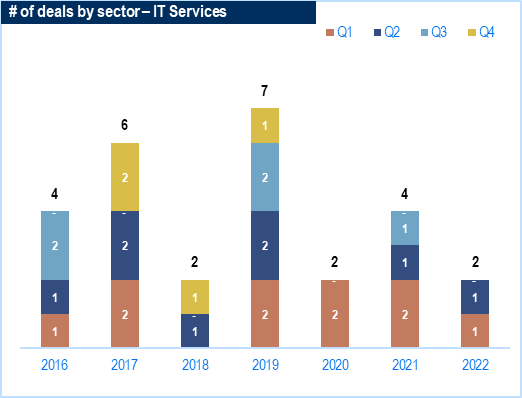

IT Services

- The demand for IT Services has declined in H1 2022, seeing a 33% fall in deal volumes with two deals in H1 2022 at USD 610Mn, ~165.2% higher than in H1 2021[43]

- Fractal joined the unicorn club with a USD 360M fund raise, the second firm in the pure-play analytics space to become a unicorn after Mu Sigma.[44] This has come on the back of increased retail market interest in the analytics space for the LatentView Analytics IPO (NSE: LATENTVIEW) in 2021[45]

- We believe that digital engineering and specialised service plays continue to be the most sought-after assets in the market, trading at a significant premium to the broader sector. Given the higher-than-average growth and larger market opportunity in these sub-segments, we expect to see sustained investor interest

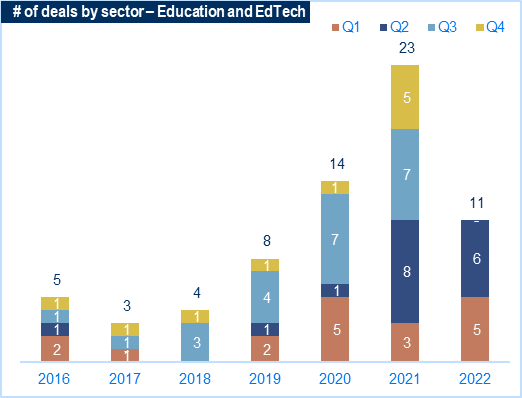

Ed-tech

- Deal activity in the ed-tech space remained mostly flat with 11 deals across both H1 2022 and H1 2021. Overall, deal value increased by 24% to USD 0.7BN (H1 2022 vs H1 2021).[47] This funding comes on the back of a stellar 2021 and an increasing focus by ed-tech players on the offline space, with a view to recapture a portion of the online education market that has moved back to the physical mode

- We believe that in the near term, ed-tech players will likely seek out more offline plays as they move to widen their offerings

- The first half of 2022 saw the rise of two new ed-tech unicorns including Physicswallah[48] - which has seen profit since inception - and LEAD School – focussing on a school based ed-tech solution to improve learning outcomes[49]

- We expect financial sponsor interest in this sector to be muted in the near-term as they seek out companies that can justify their high customer acquisition costs and expensive offerings with reasonable customer retention and a path to profitability

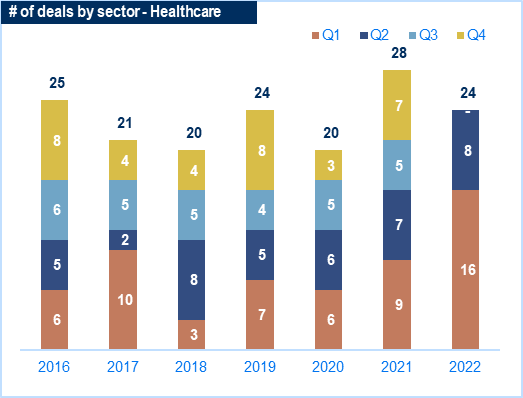

Healthcare

- Healthcare has seen a healthy uptick in deal activity with volumes 50% higher in H1 2022 than in H1 2021 (24 vs 16 deals respectively).[51] We believe this is primarily driven by a increased funding activity in the health-tech sub-sector, which accounts for a third of total transactions. However, total deal value fell by c.27% to USD 1.6BN vs H1 2021[52]

- Health-tech saw a total value of USD 300M across eight deals[53]. Consumer convenience and home healthcare delivery were key trends driving investment in this space with the likes of Docsapp/Medibuddy[54], and Redcliffe Lifetech[55] raising growth equity

- We expect continued interest in this sub-sector as a result of the Indian government’s digital health mission and the rising health consciousness of the population in the aftermath of Covid-19. Nonetheless, the key will likely be positive unit economics, which some players will find difficult

- In pharmaceuticals, buyouts have become smaller as there are not enough scaled players after the large number of buyouts in the recent past[56]. This has led to growth investments in companies such as Immuneel Therapeutics[57] and Bugworks,[58] as India tries to shift from being an outsourcing hub to an R&D hub

- In the near-term, we expect traditional pharma companies with sufficient free cash flow to raise growth funding, as they aim to capture global market share on the back of favourable policies from the Indian government[59]

- Funding in hospitals was only seen in large chains such as Asia Healthcare Holdings[60], which saw participation from Sovereign funds, as the sub-sector stabilises from its peak and offers an attractive investment opportunity[61].We expect more transaction activity in scaled-up assets - both in the form of primary and secondary investments - as they continue to grow organically and inorganically

To view sources for this publication, click here >

For information about this article read our full disclaimer >