DC Advisory's European Debt Market Monitor: Q2 2024 & Outlook

Date

September 19, 2024 • 7 min read

H1 2024 marked the busiest first half for the European broadly syndicated loan (BSL) market since 2021, with institutional loan activity reaching €134.1bn, on track to far surpass the €142.7bn recorded for the full year 2021[1].

Q2 2024 volumes rose by 46% to €79.6bn from €54.5bn in Q1, demonstrating a 326% year-on-year increase compared to the Q2 2023 volume of €18.8bn[2]. Repricing and extension activity remained the primary driver of increasing volumes, amounting to €52.6bn in Q2 2024, a 67% increase from €31.5bn in Q1[3]. Borrowers have capitalized on lower interest rates and high CLO demand to reduce borrowing costs, with margins cut by an average of 68.75 bps in 2024[4] across the European BSL market.

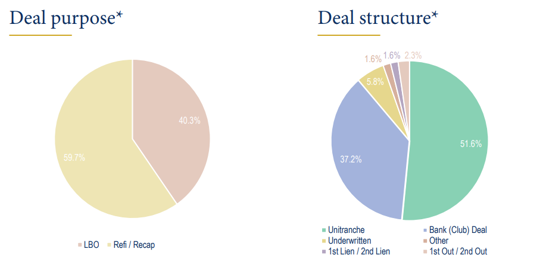

Although we saw growth in M&A activity in Q2 2024, volumes remain below 2021 levels[5]. Non-refinancing volumes surged to €17.1bn in Q2, up 120% from Q1 2024[6]. While interest rates have encouraged capital deployment, valuation gaps have kept activity below historical levels.

In our previous report, we believed sponsors with good quality assets would be increasingly willing to reset their hold period, extending maturities on their key assets, and part monetising their investment via dividend recap. This has been evident with European quarterly sponsored dividend recap loan volumes increasing to €3.87bn, the highest level since Q1 2021[7].

Despite the seasonal slowdown in July and August, the European BSL market is anticipated to maintain its momentum in H2 2024. Early Q3 2024 CLO issuances have kept demand for credits high, tightening yields, and preserving favorable conditions for borrowers.

The European Central Bank’s (ECB) 25 bps rate cut in June 2024 marked the first rate cut in five years after a sharp fall in energy prices decreased inflation to 2.6%[8]. Although a slight inflation uptick in July 2024 to 2.8%[9] may delay further cuts, the combination of lower rates, contained inflation, and an increase in economic activity offer reason for cautious optimism.

We believe this optimism may result in a bounce back of M&A activity although the timing remains uncertain, with many sponsors focusing on value creation within their existing portfolios rather than pursuing new deals. Despite sponsors utilizing other methods of distributing proceeds to shareholders, including continuation vehicles and NAV financing, the use of these has not been sufficient to distribute the required cash flows to LPs given the low levels of M&A over the last 30 months. Thus, there continues to be a significant backlog of M&A transactions.

Repricing and extension activity should remain strong as borrowers take advantage of the attractive issuance terms and yields provided by the European BSL market. We expect private credit markets will continue experiencing strong competition to maintain their market share, with a further tightening of terms noted in recent months.

Political events continue to influence market conditions, whilst the largest of these is the looming US election, the rise of the AFD in Germany[10] and uncertainty in France[11] should also be considered.

For more information about this publication, read our Debt Market Monitor disclaimer >

References

*Unless otherwise indicated, all tables, data and statistics provided in this piece, including with respect to deal activity, have been collected via the August 2024 DC Advisory Lender Survey, subject to the limitations of described below.

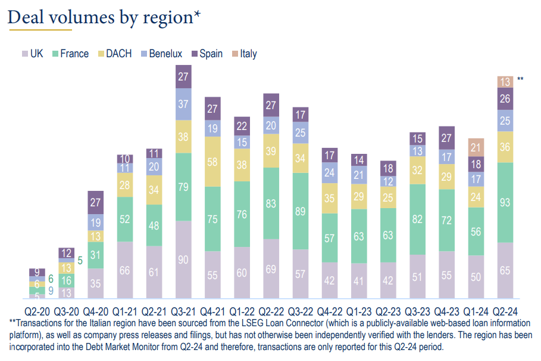

**Transactions for the Italian region have been sourced from the LSEG Loan Connector (which is a publicly-available web-based loan information platform), as well as company press releases and filings, but has not otherwise been independently verified with the lenders. The region has been incorporated into the Debt Market Monitor from Q2-24 and therefore, transactions are only reported for this Q2-24 period.

The August 2024 DC Advisory Lender Survey: (DC Advisory’s independent survey of 98 European banks and direct lenders. which was completed in August 2024 and conducted across UK, France, Germany, Austria, Switzerland, Spain, Belgium, Netherlands and Luxembourg (referred to herein as the “The August 2024 DC Advisory Lender Survey” or the “Survey”). Any such data, including league table data referenced herein is limited to the data provided by the Survey participants and is not meant to constitute definitive market data. The banks and lenders selected for the Survey are based on those that are most active in the market, and that DC Advisory interacts with the most. Accordingly, the Survey participants do not constitute an exhaustive list of banks and lenders who may have been active during the period addressed by the Survey. Comparisons to deal activity or other statistics from prior quarters or other periods are calculated by comparting the results of the Survey to the results from DC Advisory Lender Survey corresponding to the prior period, subject to the same limitations described above.)

[1] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[2] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[3] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[4] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[5] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[6] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[7] LCD Pitchbook European Credit Markets Quarterly Wrap Q2 2024

[8] https://ec.europa.eu/eurostat/en/web/products-euro-indicators/w/2-20082024-ap

[9] https://ec.europa.eu/eurostat/en/web/products-euro-indicators/w/2-20082024-ap

[10] https://www.lemonde.fr/en/opinion/article/2024/09/02/the-worrying-rise-of-germany-s-far-right_6724463_23.html

[11] https://www.ft.com/content/d895e5e6-e921-4c47-98f4-b907ce91c4d7

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.