DC Advisory's US sector specialists share their observations of M&A activity in Q2 2021 and the key trends expected to drive deal flow.

Sector Commentary

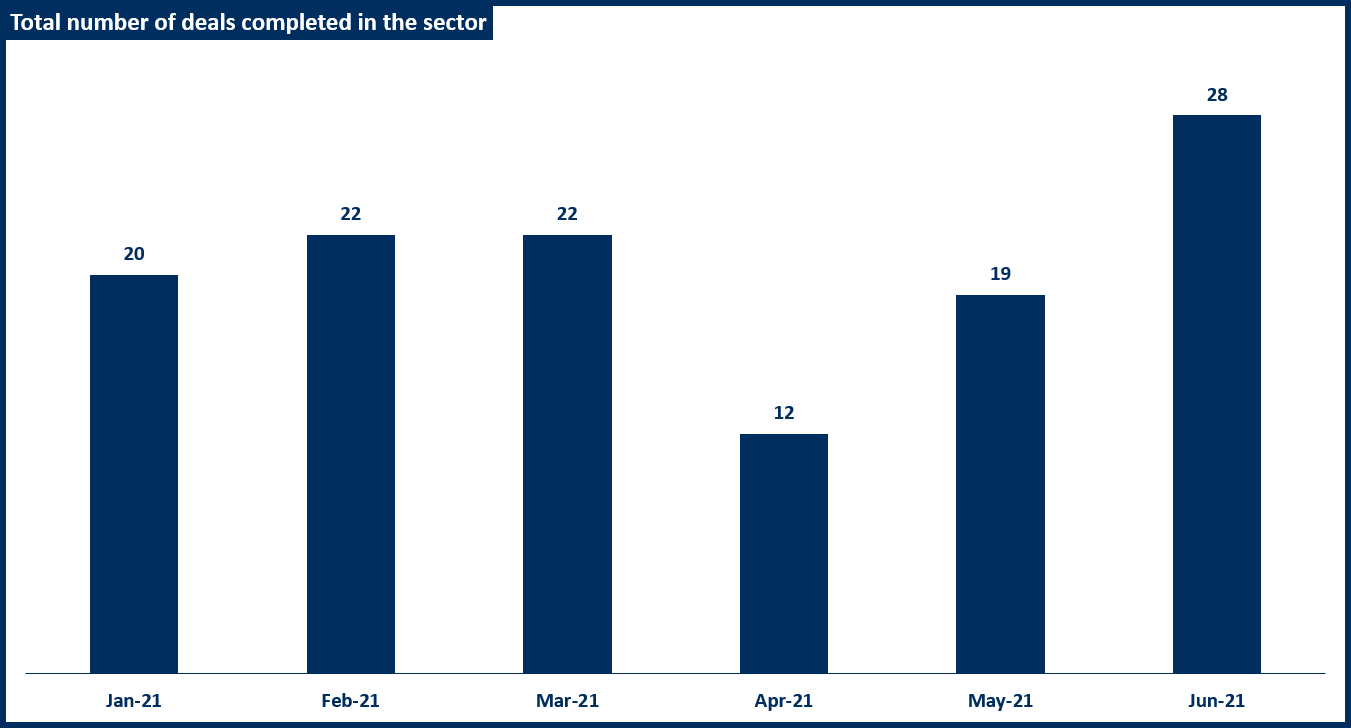

Aerospace, Defense & Government Services

The Biden Administration announced that the remaining 2,500 US troops would be withdrawn Afghanistan by September 11, 2021[1] in a continuation of the broader strategic shift toward addressing near-peer adversaries such as China and Russia. As a result of shifting U.S. Department of Defense (DoD) priorities, large contractors are likely to continue portfolio shaping via mergers and acquisitions to divest non-core businesses while also seeking to gain increased exposure to faster-growing segments of the market.

The Biden Administration also issued an executive order intended to improve information technology (IT) and operational technology (OT) security at federal agencies and industry partners[2]. This has led to additional requirements being mandated for contractors while those with existing cybersecurity capabilities and / or exposure to the Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency (CISA), which has been given increased authority, are likely to benefit from increased demand. Large strategics and mid-sized contractors without an existing presence at CISA are likely to seek acquisition opportunities to gain a foothold with the agency

Digital transformation, software development, security and operations (DevSecOps), simulation-based training, and advanced weapons systems remain high priority capability areas, as the DoD seeks to maintain readiness while spending efficiently; many contractors with these capabilities are seeing both above-average revenue growth and acquisition interest at premium valuations.

Congressional negotiations regarding the 2022 budget, infrastructure bill and potential increases to both corporate and capital gains taxes are ongoing and being watched closely by industry participants. Potential increases to capital gains taxes[3] have served as an impetus for many companies to launch sales processes with the intent to close before tax changes go into effect. The M&A market has been and will continue to be very active as a result.

Business & Tech-Enabled Services

Current M&A pipeline in the business services sector remains robust, driven by both strategic and private equity activity – as demonstrated by transactions such as H.I.G. Capital’s anticipated acquisition of Oxford Global Resources from ASGN[4], EQT’s acquisition of PRO Unlimited and Kelly Services acquisition of Softworld[5]

There is a strong buyer interest across almost all subsectors with companies that have scalable business models, a tech-enabled element, or a loyal customer-base, drawing most demand

PEs are actively seeking bolt-ons to bolster existing platforms as they look to add scale or expand vertically, which we expect to continue in 2021 and beyond as they continue to look for growth beyond what is possible organically

Labor shortage remains one of the biggest constraints to growth for people-based service businesses and is expected to remain so for at least the remainder of 2021 as economic conditions remain strong[6]

Source: ‘Total number of deals completed by sector’, Mergermarket, 30 June 2021

Travel & Hospitality

Transaction activity in Q2 2021 was down from Q1 2021[7], however transaction make-up shifted more heavily towards strategics. Industry consolidation continues to be driven by the pandemic, however Q2 has also seen recovery in the traditional pre-Covid segments (Airlines, Hotels, etc)[8], given the lockdowns easing

Hotels were more focused on expanding into Asia during Q2 2021, hinting at more growth and expansion for smaller short-term rental and online booking companies domestically.[9] More attention can be given to these companies, as they establish marketing materials to advertise their cheaper prices compared to the companies that dominate the sector

Domestic travel has risen substantially in Q2 2021[10] and it is on track to reach pre-pandemic levels by the end of this year or early next year. The month of May recorded 42% of Americans travelling[11]. At the current rate, this will be one of the strongest summer travel seasons on record

The resurgence and improving financial performance of the Travel & Hospitality industry makes industry players more ideal acquisition targets, especially for financial sponsors and sponsor-backed companies

The labor shortage for hotels suggests that the sector is recovering faster than anticipated. Several hotels have limited guest capacity to maintain adequate service levels for customers. Similarly, short term rentals are increasing the amount of hosts on their platforms to ensure a sufficient number of properties for the growing demand[12]

Local travel continued its significant growth through Q2 2021[13]. Daily car rental costs jumped to a record high[14] and traffic volumes surpassed that of 2020 in the same period[15]. We expect a similar trend moving forward, subject to any potential impact of the new delta variant, as the season progresses and vaccination levels rise.[16] This data shows an opening for an increase in M&A activity for alternative car rental service companies

Leisure travel continues to outpace business travel which remains at low levels due to only 21% of workers returning to office[17] – even with a jump from 17% to 45% in vaccination levels between Q1 2021 and Q2 2021[18]. However, this trend may change by the end of the year with 87% of workers expecting business trips by Q4 2021[19]

The new era of travel and hospitality has sharpened its teeth, proven its value throughout Covid and is ripe for consolidation as larger incumbents seeking to adapt to shifting trends

Source: ‘Total number of deals completed by sector’, Mergermarket, 30 June 2021

Education & EdTech

Businesses in the EdTech sector continues to be in high demand as the pandemic environment has dramatically accelerated digital transformation and online adoption rates[20]

Concern persists amongst educators that prolonged periods of remote learning have had a significant impact on students’ academic and emotional well-being, and have increased the disparity of educational outcomes.[21] We believe this concern will trigger more investment in the space, as Education companies look to overcome any potential problems through M&A activity of complementary service providers

The American Rescue Plan Act of 2021, which was passed on March 11 2021, has allocated over $120 bn of funding for K-12 schools[22] reducing the fear in the near-term of tightening public school district budgets

M&A activity in the sector remains robust, driven in part by the availability of capital and industry consolidation

Despite the high valuation environment, social impact investors continue to be active participants in the sector

Source: ‘Total number of deals completed by sector’, Mergermarket, 30 June 2021

Industrials

M&A activity levels continued to increase into Q2 of 2021, with deal volume up sequentially relative to Q1[23]. We believe this is due to strong economic and commercial activity levels, and favorable financing rates as companies look to add growth via acquisitions

Corporate divestiture activity is continuing to increase as industrial corporates focus on portfolio positioning over the medium - long-term

We believe there are strong levels of buy-side interest in acquisitions from corporates and private equity, both within the US and abroad, again due to strong level of commercial and economic activity, and favourable financing rates

Source: ‘Total number of deals completed by sector’, Mergermarket, 30 June 2021

Media & Telecom

This edition, we focus on information services:

Recent share price performance and valuation multiples for public Information Services companies reflects strong investor confidence in the sector – at the end of Q2 2021, the Information Services composite grew 33.2% since the end of Q2 2020[24] and 16.1% since the end of Q1 2021[25]. This has contributed to a significant uptick in M&A activity, as sellers look to capitalize on record high valuations

Momentum in the Information Services sector carried over into the M&A market, with 66 completed transactions during Q2 2021[26]- a significant uptick relative to the 47 transactions completed in Q2 2020 (~40% increase)[27]. The increased M&A activity in the Information Services sector is especially pronounced among sponsor-backed deals, where private equity firms are either looking to sell portfolio companies or apply dry-powder

As ESG definitions continue to evolve, the demand for high-quality ESG solutions has spurred both organic and inorganic activity, highlighted by:

JPMorgan & Chase’s acquisition (agreement in principle) of OpenInvest[28], a provider of value-based, ESG financial advisory and management solutions, and:

Among the broader Information Services sectors, Governance, Risk and Compliance (GRC), Financial Information and Real Estate & Construction experienced heightened deal flow, including the ~$6 billion acquisition of CoreLogic (NYSE:CLGX), a global property information, analytics and data-enabled solutions provider, by Stone Point Capital and Insight Partners[30]. While these deals reflect emerging themes arising out of COVID, they are representative of broader secular trends pertaining to the demand for unique datasets and associated analytics. We expect these trends to continue to persist, leading to ongoing consolidation across the information services landscape

Source: ‘Total number of deals completed by sector’, Mergermarket, 30 June 2021

Real Estate

More consolidation is likely as big players race to become a one-stop shop for home buying and selling[31]

The residential real estate market remains highly active despite historically low inventory

Only 468,000 homes were for sale in the U.S. in the first couple months of 2021, which is roughly half the supply from the same time last year[32]

Brokerage companies and listing platforms will likely face increasing competition to represent and list homes

Many companies will likely be looking to raise capital or transact in this sector to keep up with the highly active market and remain competitive

A lot more people want to move home and interest rates are dropping, which is offering financing to people who hadn’t previously considered purchasing homes[33]. We believe these lower interest rates are driving M&A demand in the Real Estate Tech sector for digital financing solutions

The pandemic is driving innovation for digital and tech-enabled solutions from financing, to digitally closing mortgages, to virtual showings, ramping up digital infrastructure in Q2 2021[34]. We believe this will increase M&A activity in the space - we expect the trend to continue as many companies will be looking to raise capital to support their growth and technological advancements

The move towards hybrid or permanently remote work models drives the addition of co-working areas in rental and condo buildings and changing layouts of units to include home offices[35]. Large players in the real estate space may be looking to acquire or consolidate construction companies and vendors due to increasing demand for these services

We expect M&A activity in the Real Estate Tech space this year to remain strong as the real estate market remains active and pandemic uncertainty continues to drive innovation[36]

Tech & Software

This edition, we focus on customer interaction management (CIM) within the Technology & Software space

Capital investment in leading-edge customer interaction technologies, including sales, marketing, and efforts for ‘inbound’ and ‘outbound’ technologies – for example Twilio’s acquisition of Zipwhip[37] - have driven market adoption and, as a result, M&A activity, among vendors looking to provide the broadest portfolio of offerings to further differentiate and compete

Technological enablement and demographic shifts are driving omni-channel engagement, including self-service chatbots, text messaging[38], AI-driven virtual assistants via conversational intelligence, and social media channels, among others, also increasing deal activity in the space[39]

The Covid-19 pandemic has shone a spotlight on the relevance of CIM, which has been reflected in many CIM incumbents, heightening the ability to work remotely or deal with customers in a remote manner

The evolution of the CIM market continues to consolidate across all the key verticals, including classic customer relationship management (CRM), workforce engagement management (WEM), business intelligence (BI) & analytics, and traditional contact center markets. We believe this will lead to M&A activity increasing as vendors look to add capabilities across a number of key functions and markets

This evolution and its drivers have created a massive market, projected to reach over $105 billion by the end of 2024 (Combined segments represent Gartner forecast for Customer Experience & Relationship Management market worldwide: the largest and fastest growing software market tracked by Gartner)[40]

From an M&A standpoint, CIM valuations have been steadily rising over the past 6 years with the average strategic multiple paid in 2020 being 6.5x EV LTM / Revenue[41]

Many public companies in the sector have traded at near or above 52-week highs in 2021, driving CIM strategic multiples even higher, for example, Microsoft’s acquisition of Nuance (13.6x revenue)[42]

Regardless of the increasing cost to acquire CIM assets, large PE firms continue to show interest in the space due to its mission critical nature and strong future growth potential

Source: ‘Total number of deals completed by sector’, Mergermarket, 30 June 2021

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists: