DC Advisory’s European Mid-Market Private Equity Round-Up: Q4 2019

Date

January 15, 2020 • 1 min read

October - December 2019

January 2020

DC Advisory presents our latest European update for mid-market activity for the Q4 2019 period.

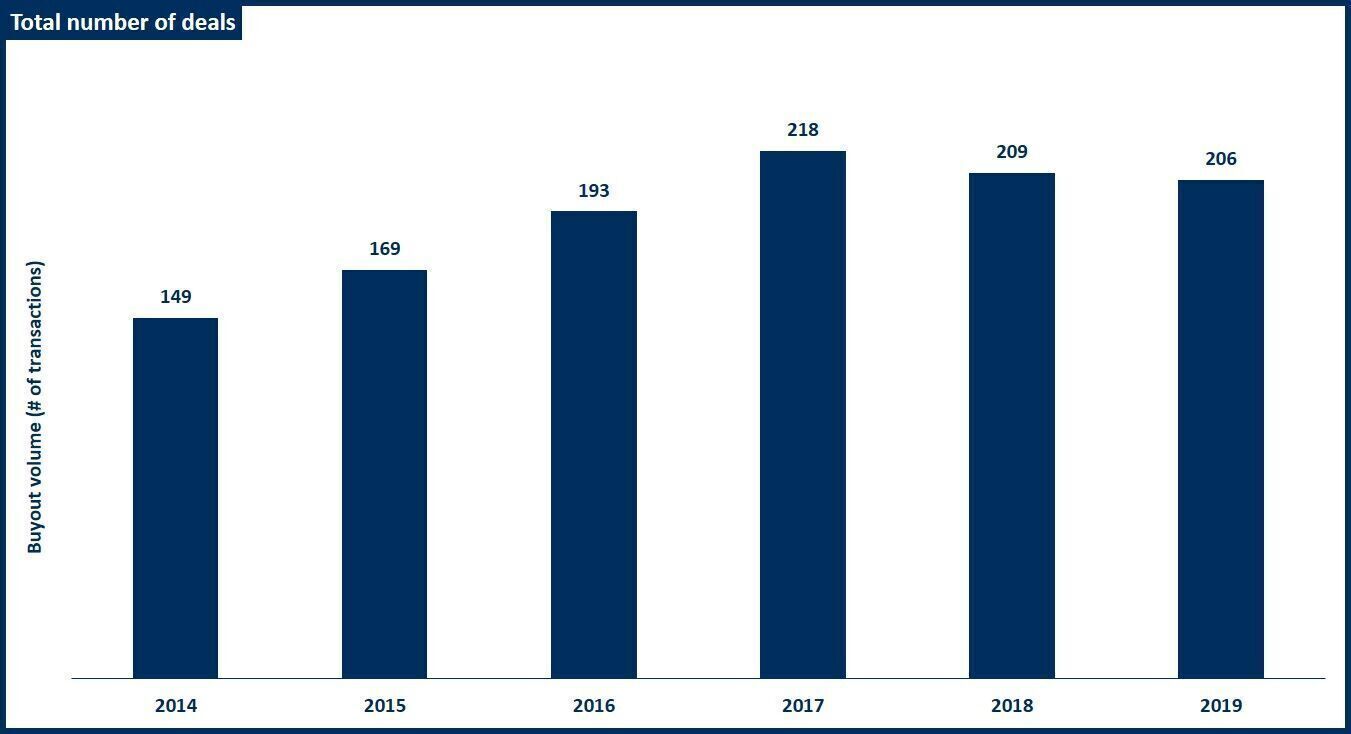

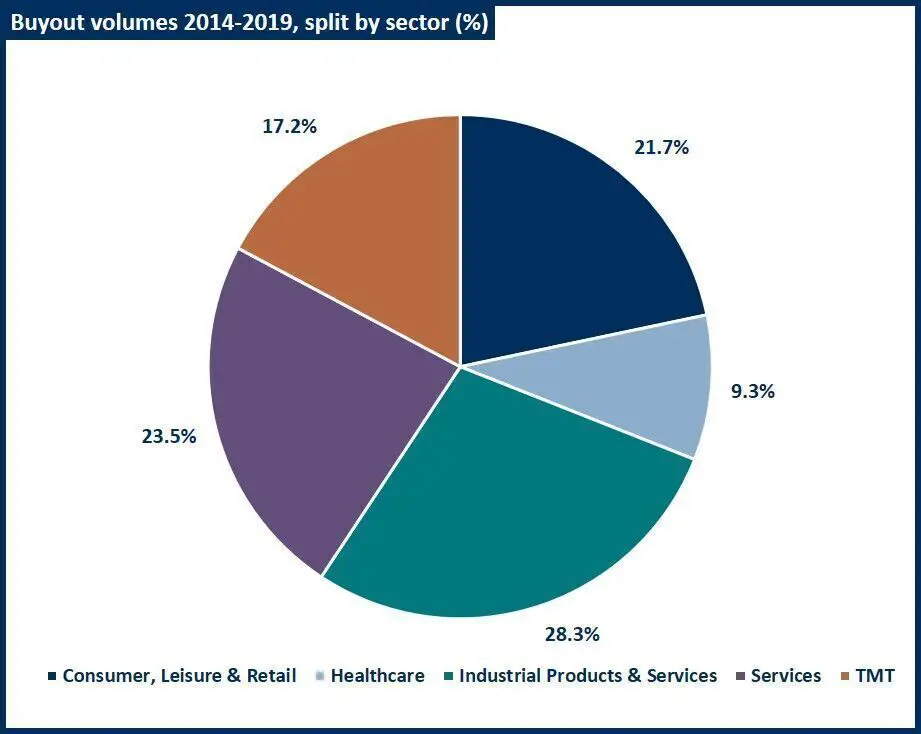

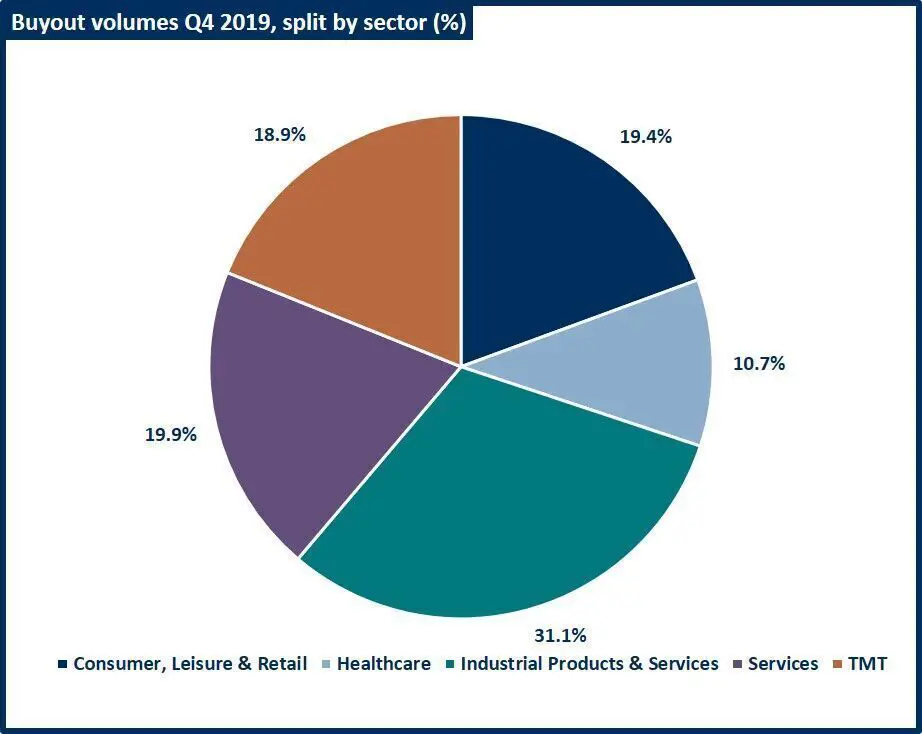

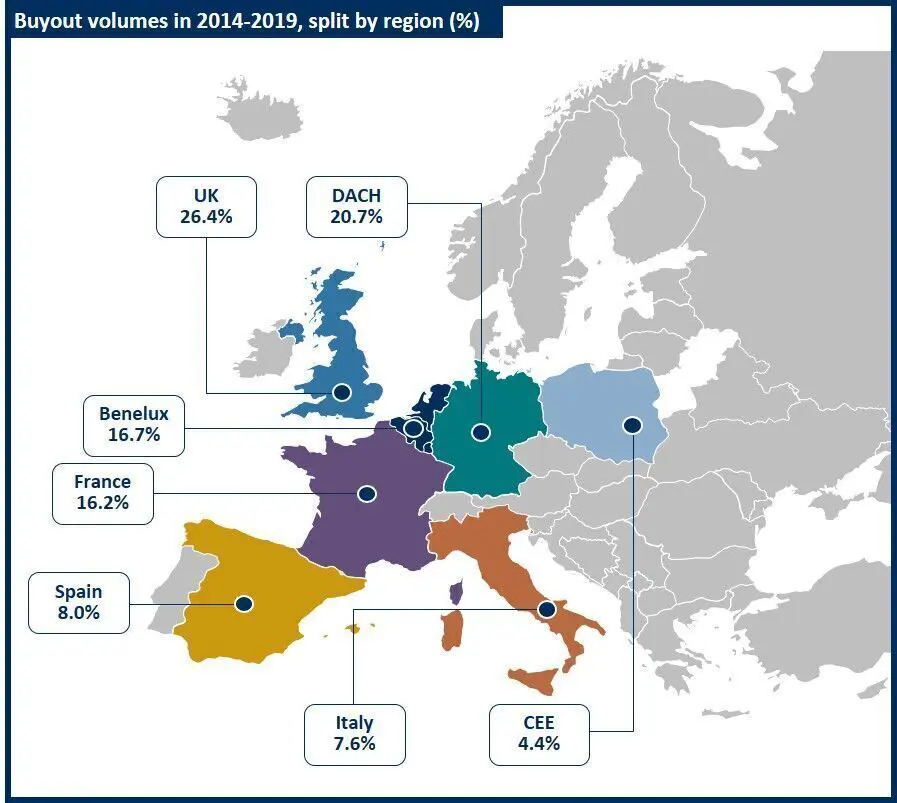

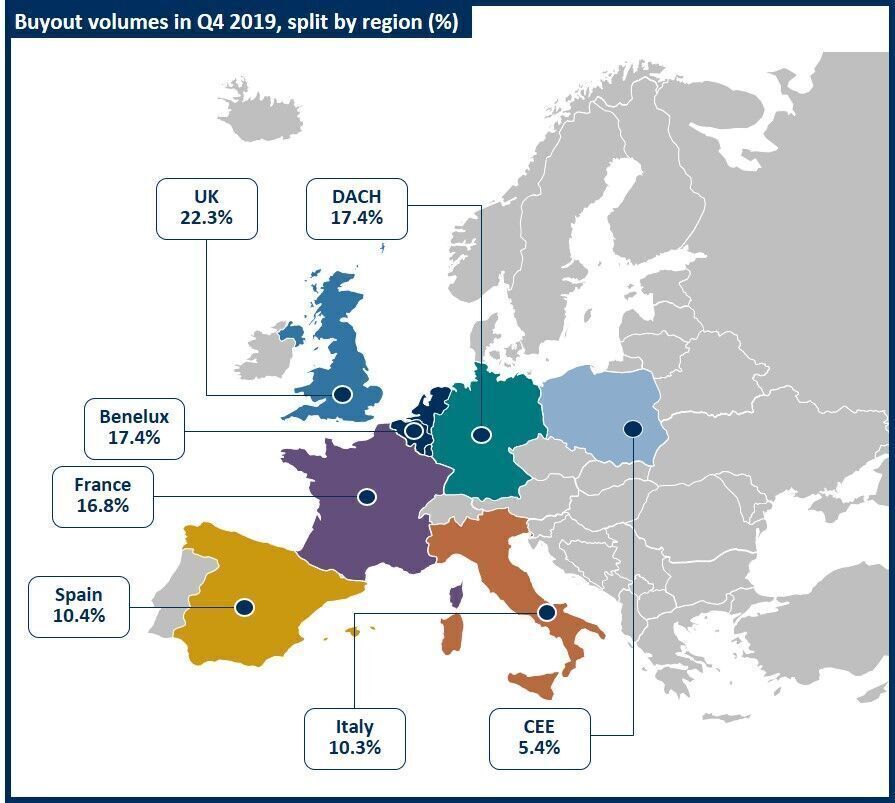

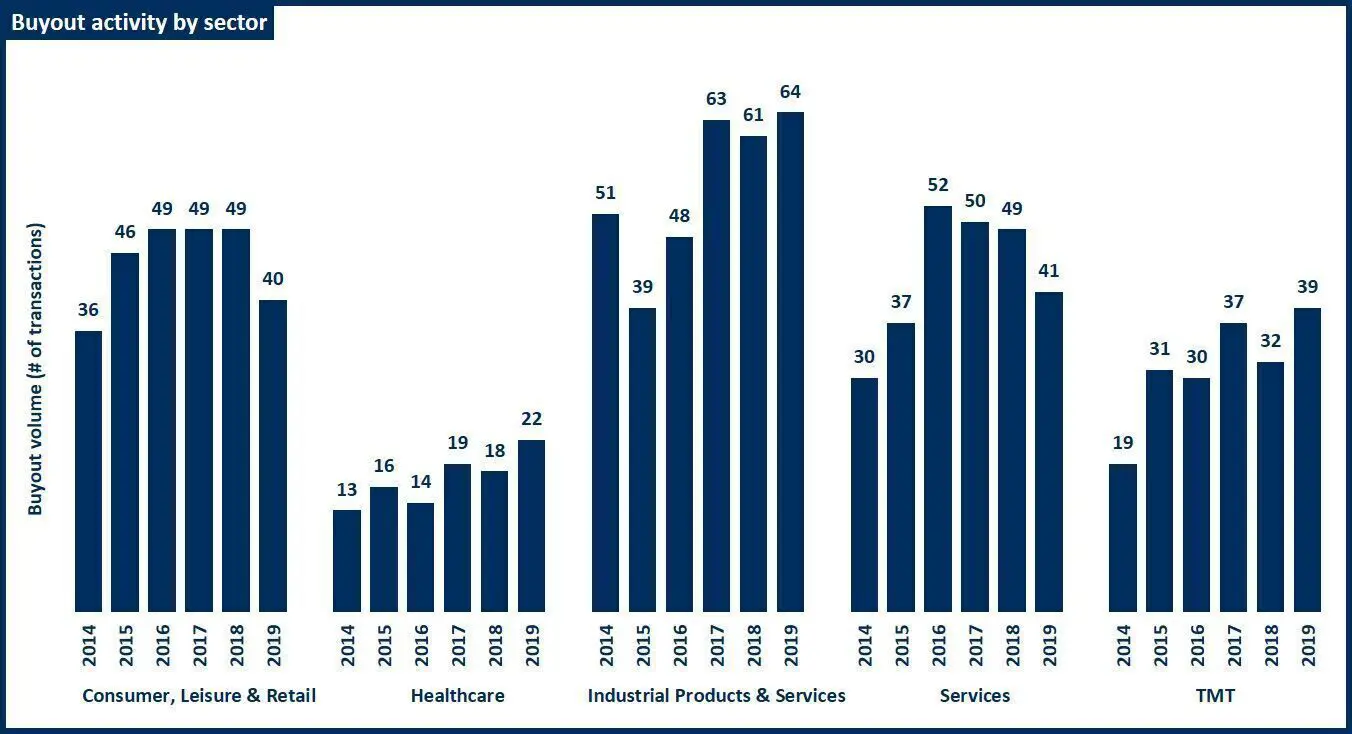

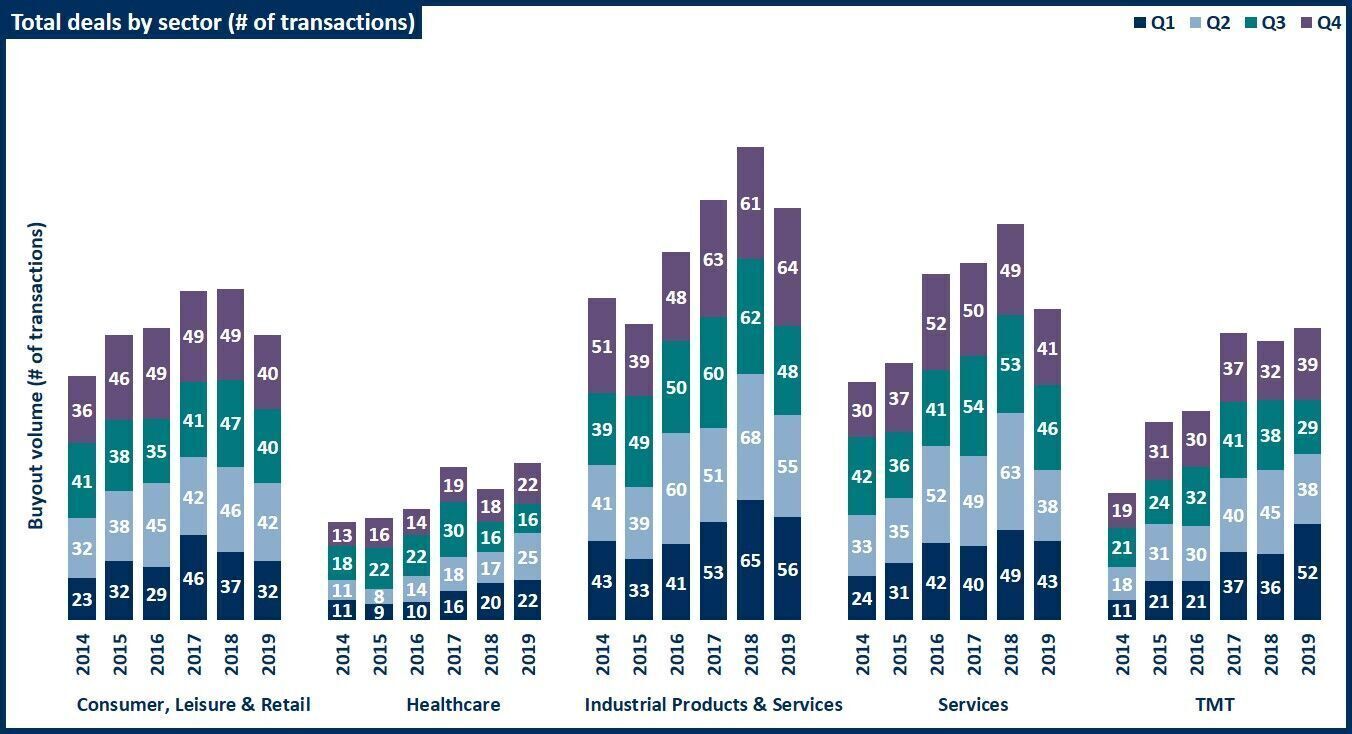

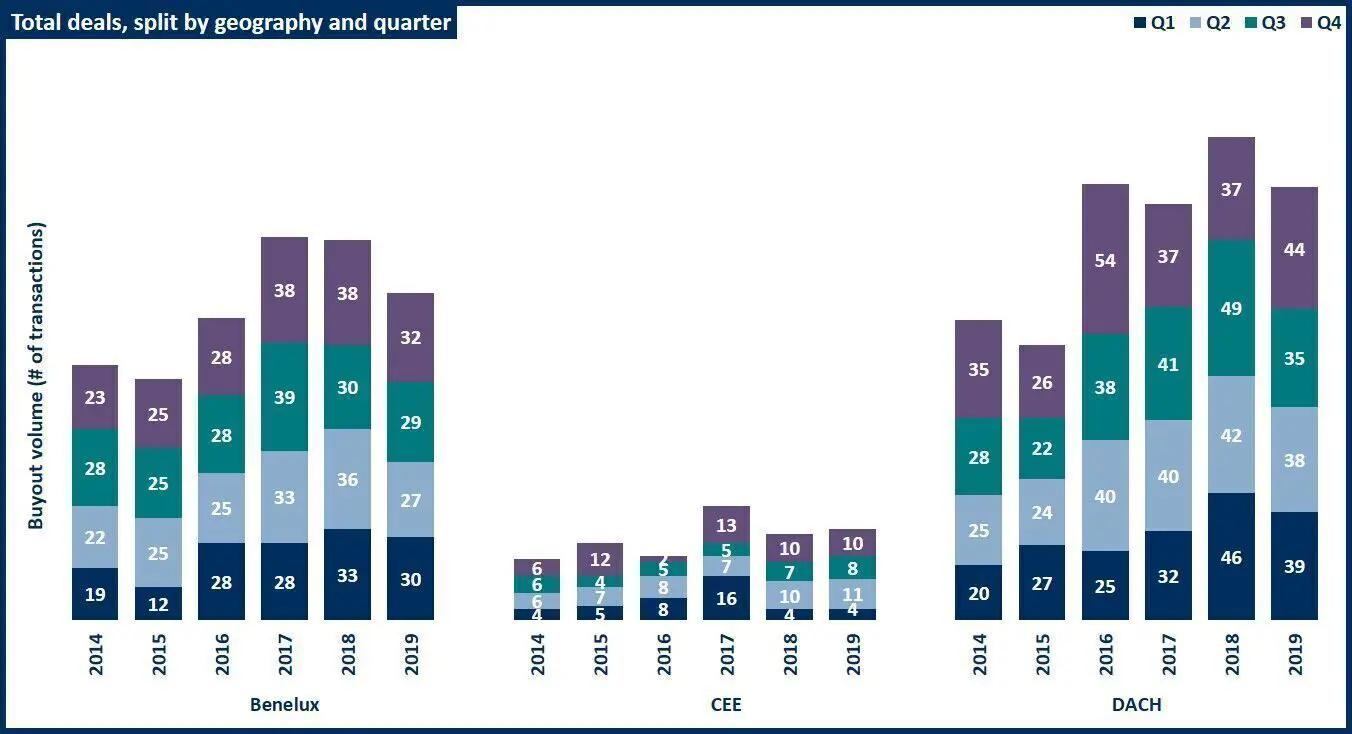

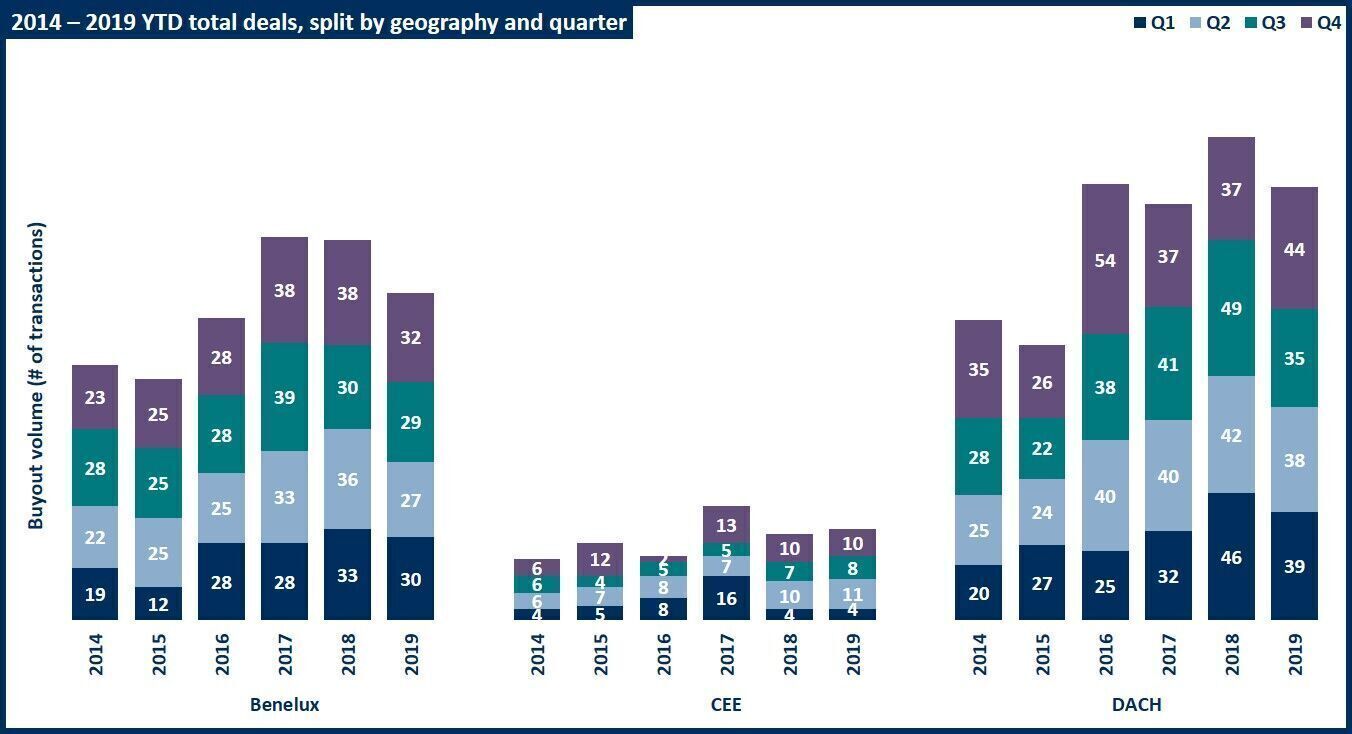

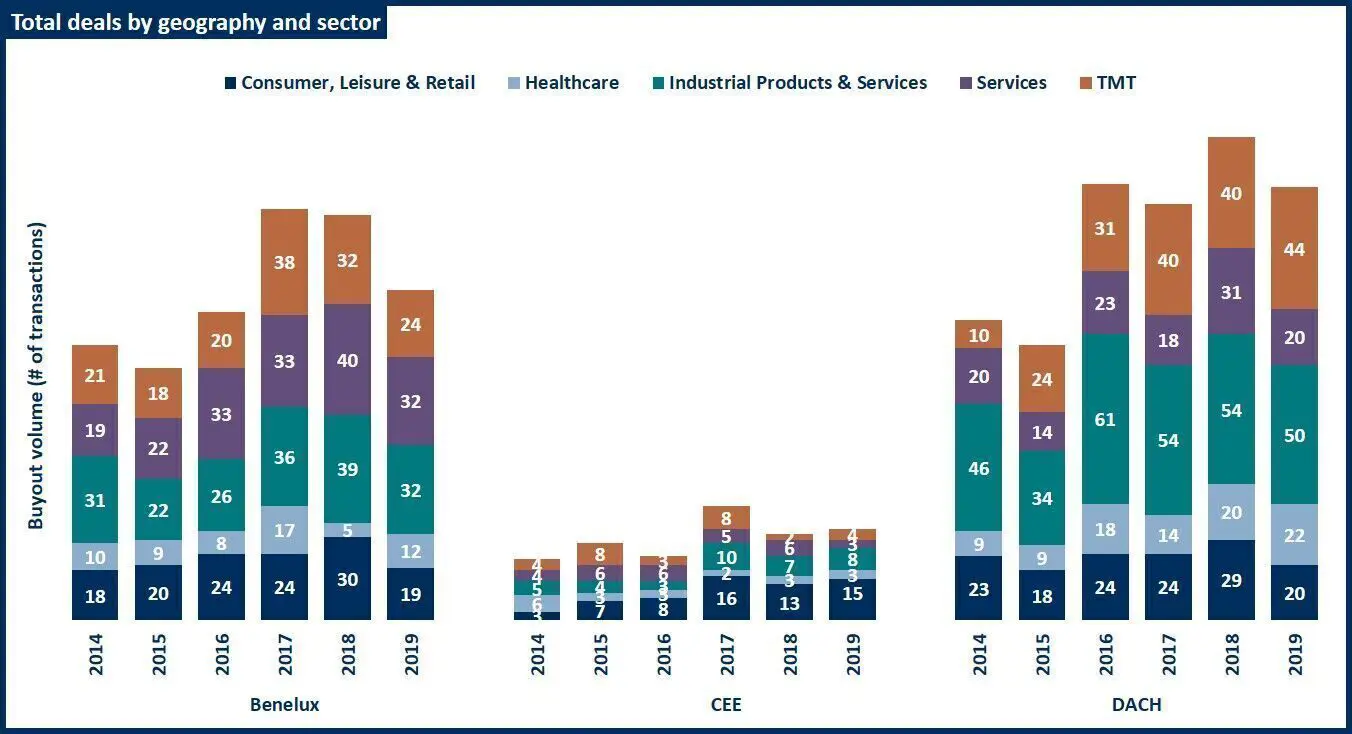

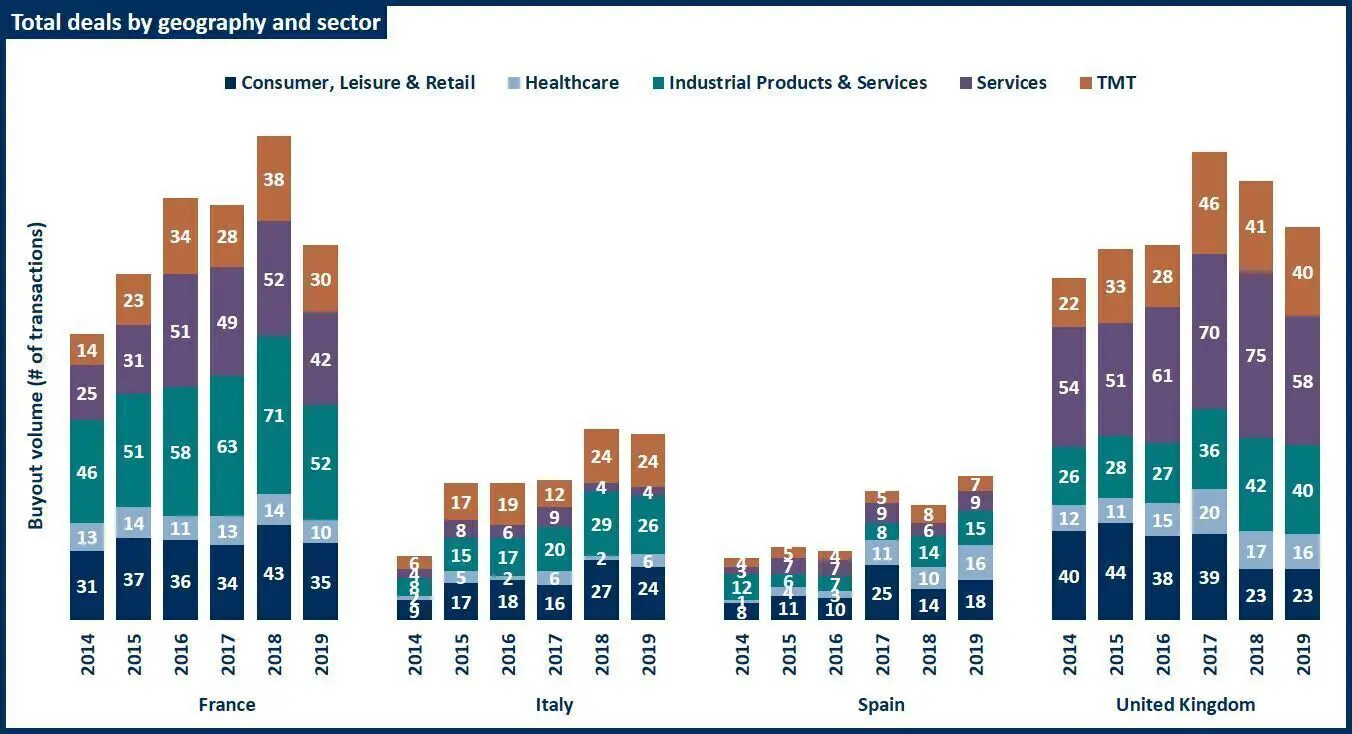

European deal activity experienced an uptick in the final quarter of 2019 – consistent with the 2018 trajectory. This consistency has predominantly been due to the increased popularity in the smaller markets of France and Spain, which has offset the declining deal volume in the UK throughout 2019. In terms of private equity transactions, the TMT and Industrials sectors continued to attract investors during Q4 (21% and 5 % increase YOY for Q4, respectively), illustrating the growing trend towards tech-enablement in all industries. In comparison, the Consumer and Services sectors experienced a marginal decline in Q4 buyouts.

Much of Europe’s deal activity during this politically unsettled period was in its blossoming start-up scene. Total investment value for the year was $30bn (a massive 40% increase on 2018 levels) with over 2,300 start-ups invested into during the year – which is perhaps a consequence of more mid-market private equity houses raising specialist funds with which to invest in young technology groups.

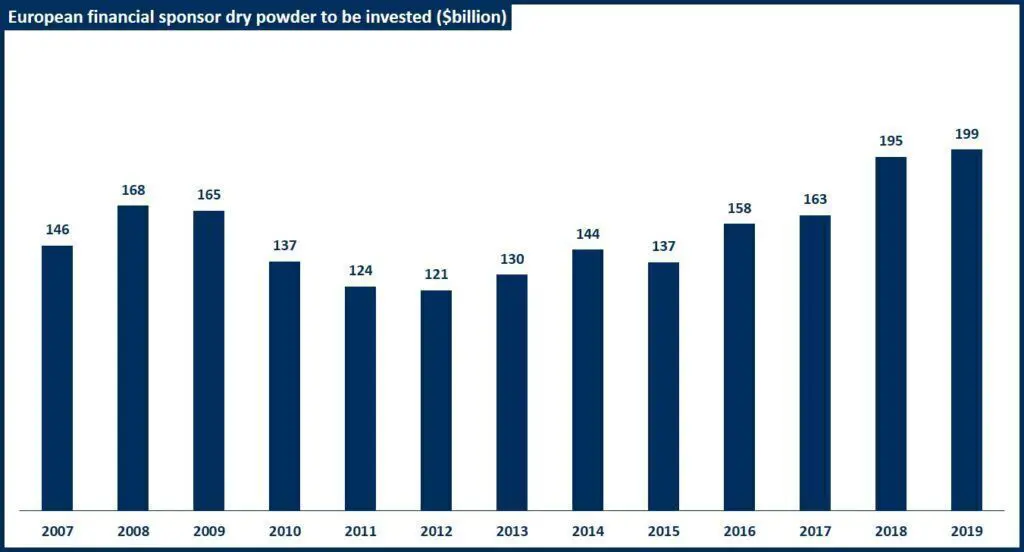

With dry powder in the European market totalling close to $200bn, deal values across the continent have remained robust, with investors competing to acquire quality assets. This, coupled with greater numbers of non-European investors showing interest in European businesses (to take advantage of low ECB interest rates and to expand geographical footprints), suggests that the outlook for 2020 deal activity is promising.

Your message has been received by DC Advisory so you'll hear back from us soon.

We collect your personal data if you sign up to receive news or get in touch with us. This is collected by third-party firms on our behalf. We have three separate lists:

Your message has been received by DC Advisory so you'll hear back from us soon.